ESOP Valuation Firm Malaysia

A Practical Guide for Professionals Navigating Employee Stock Option Plans – ESOP Valuation Firm Malaysia

Introduction to ESOP Valuation Firm Malaysia

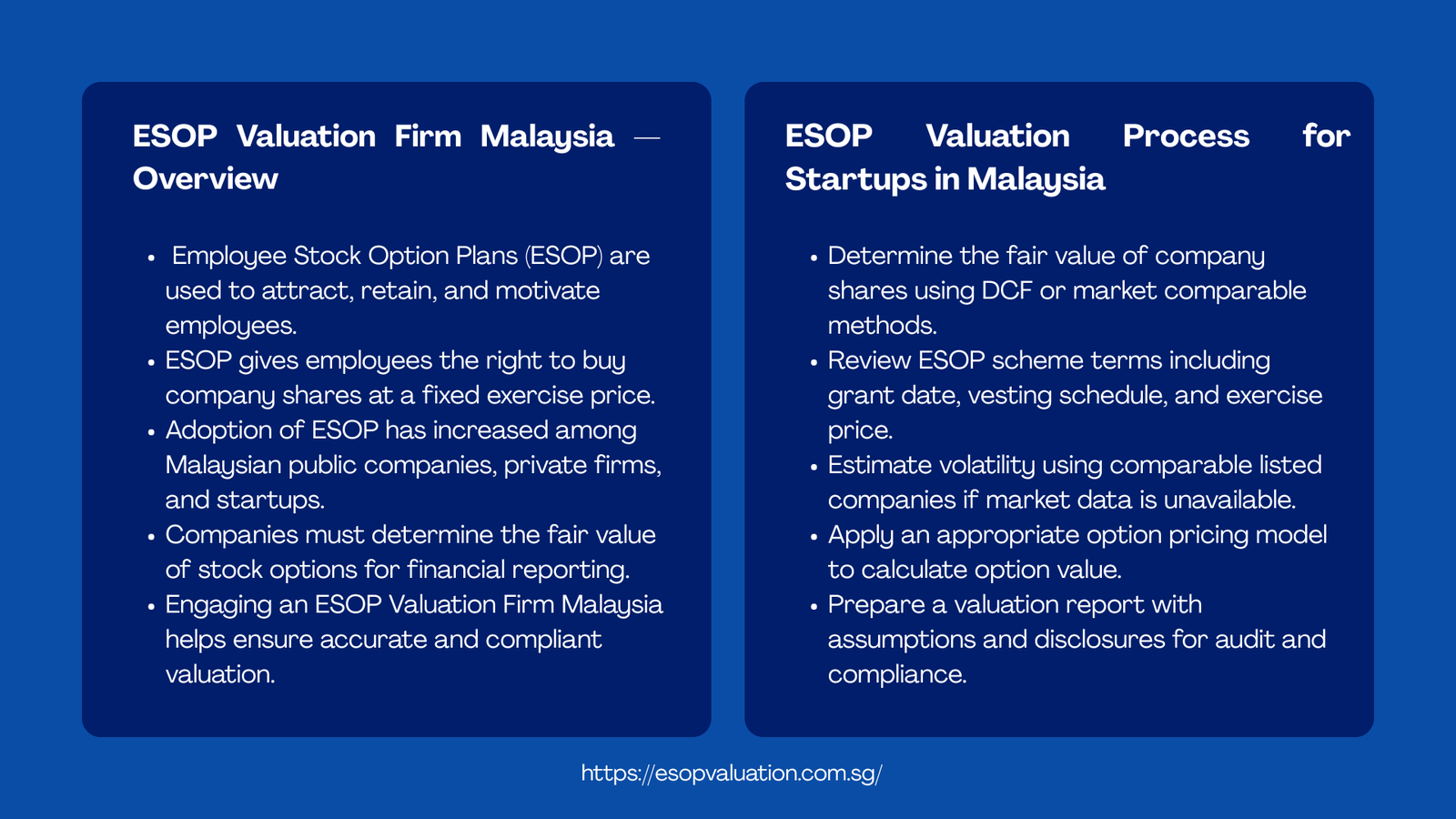

Employee stock option plans, which are also referred to as ESOP, have emerged as one of the more significant instruments firms have been relying on in attracting, retaining and aligning talent with business performance. Their application has increased significantly in the last ten years not only by publicly listed companies but also by a growing number of small enterprises and technology-based start-ups in Malaysia. But even though popular, the process of valuing employee stock option plans in Malaysia remains one of the most unfamiliar spheres to most of the professionals joining the corporate or financial arena.

To the junior to mid-level professionals in the field of finance, human resources, corporate secretarial or legal, the knowledge of the valuation of ESOPs and the importance of the valuation of ESOPs can make significant contributions towards the quality of the work you can produce. This knowledge of ESOP valuation, whether you are engaged in financial reporting, a due diligence exercise or are just struggling to comprehend your own compensation package, will provide a practical advantage.

This paper discusses the major considerations, regulatory framework, valuation techniques, and practical issues of ESOP valuation in Malaysia. It has been authored to individuals who are not so familiar regarding the subject but are willing to take it seriously. No high level financial modelling experience is needed – only desire to know how it works at the grass roots level.

The importance of ESOP Valuation to Malaysian Companies – ESOP Valuation Firm Malaysia

An ESOP fundamentally grants the employees the right to acquire shares in their own company at a fixed price after meeting some conditions, typically a vesting period, which is termed as exercise or strike price. The worth of such a right will be determined by numerous factors as well as the prevailing share price, the exercise price, the duration of the option, and the market volatility. Companies need to determine a fair value of these options upon granting them to accountants and regulatory reasons.

In Malaysia, Malaysian Financial Reporting Standard 2 or MFRS 2 which is very similar to IFRS 2 is the key accounting standard in this country. In MFRS 2, the share-based compensation, such as stock options, should be treated as an expense in the income statement of the company with a fair value of options at the grant date. This is not optional. This is regardless of whether your company is publicly traded on Bursa Malaysia or it is privately owned, and thus, prepares audited financial statements.

It has important practical implication. When a business gives out a high number of options when the underlying share value is high, then the associated cost can have a significant impact on the reported profit. Similarly, a wrong or unsubstantiated valuation is prone to question by auditors, the Securities Commission Malaysia or even investors. This is the reason why most companies, particularly the ones that lack the in-house valuation capacity, resort to specialist ESOP valuation services for private companies in Malaysia.

Requirements and Methods : ESOP Valuation Firm Malaysia

Prior to choosing an approach, one can benefit by appreciating what the ESOP valuation requirements and methods in Malaysia in fact require of a compliance standpoint. MFRS 2 stipulates that equity-settled payments in the form of share option should be measured at fair value on the grant date by an option pricing model. The standard does not recommend one of the models but anticipates that the methodology applied is representative of the particular characteristics of the instrument under valuation.

The Black-Scholes model, the Binomial (lattice) model, and Monte Carlo simulation are the three most popular models used in the Malaysian practice. The most common is the Black-Scholes, which is simplified and has a proven methodology. Nevertheless, it is limited, especially when it comes to options where the vesting is non-standard, there are performance obstacles or early exercise ability. Preferably in such scenarios, a Binomial or Monte Carlo method is more acceptable or justifiable.

Table 1: Popular Valuation Techniques and their Uses – ESOP Valuation Firm Malaysia

| Method | Best Used For | Key Input | Complexity |

| Black-Scholes Model | Standard employee options | Volatility, risk-free rate | Low–Medium |

| Binomial/Lattice Model | Options with vesting conditions | Exercise patterns, market data | Medium–High |

| Monte Carlo Simulation | Complex performance vesting | Scenario modelling | High |

| Discounted Cash Flow | Underlying share valuation | Projected cash flows, WACC | Medium |

| Market Comparable | Benchmarking share price | Peer company multiples | Low–Medium |

Irrespective of the model adopted, there are five major inputs that should be estimated or compiled and they include the current fair value of the underlying share, the exercise price, the interest rate which is risk free, expected volatility of the share price, and the expected life of the option. In the case of listed companies, some of these inputs can be observed based on the market. In the case of private companies, greater judgment should be done and more documentation should be done.

5 Steps : ESOP Valuation of Startups in Malaysia – ESOP Valuation Firm Malaysia

Startups take a very complicated stance with regard to ESOP valuation. In most cases, they do not have the trading history, audited earnings and other such market data that makes it comparatively easy to value established businesses. Knowing how to calculate ESOP valuation for startups in Malaysia is a process of moving through these gaps in a systematic way and having clear assumptions.

The procedure is generally applicable and takes five major steps:

Step 5 — Determine the Fair Value of the Underlying Shares. In the case of a startup, which is not yet listed, this needs a separate shares appraisal, which is usually by DCF model or a market comparables method. The ESOP valuation model takes this step output as the direct input of the current share price.

Step 2 — Determine the Option Terms. Collect formal ESOP scheme documentation, which contains grant date, exercise price, vesting schedule, performance conditions (where applicable) and option expiry. The words constitute the framework of the instrument in question.

Step 3 — Estimate Volatility. Since a startup does not have any historical share price information, the volatility has to be approximated using proxy information – usually the historical volatility of similar listed companies within the same industry and geography. This will involve research and judgment and the chosen comparables need to be recorded.

Step 4 — Implement the Selected Pricing Model. Having everything above, use the chosen option pricing model, most commonly the Black-Scholes in the process of granting a simple one, or a Binomial model when the terms of vesting are complicated. The model gives a fair value of each option at the grant date.

Step 5 — Prepare Valuation Report and Supporting Disclosures. Formally establish all assumptions, inputs and methodology in a formal valuation report. This report is presented to the auditors of the company and the foundation of the MFRS 2 expense recognised in the financial statements. The failure to collect and record complete reports is a frequent source of audit problems.

Table 2: ESOP Valuation Engagement Stage-by-stage Process Flow – ESOP Valuation Firm Malaysia

| Stage | Activity | Key Documents / Inputs | Responsible Party |

| 1 — Engage | Appoint valuation firm & define scope | ESOP scheme rules, share structure | Company + Valuer |

| 2—Data Gather | Collect financial and operational data | Audited financials, cap table, forecasts | Company |

| 3 — Analyse | Apply valuation model & assumptions | Volatility data, discount rate, grant terms | Valuer |

| 4 — Report | Prepare valuation report with findings | Draft report, management review | Valuer + Company |

| 5— Compliance | Submit to auditor / regulator as required | Final report, MFRS 2 disclosures | Auditor / Company |

Practical Applications: The Forms of Valuation in the Real World – ESOP Valuation Firm Malaysia

As an example of a Malaysian fintech company, the company has announced an ESOP in its Series A round, providing 25 key employees with an exercise price of RM 2.00 per share. The company did not have a listed share price and thus the valuation company was contracted to first establish the fair value of the company shares- coming up with the RM 3.50 per share based on DCF model which was benchmarked to other regional comparable fintech companies. Application of Black-Scholes model as above with expected option life standing four years and proxy volatility calculated based on three listed Malaysian fintech peers indicates that the fair value per option is RM 1.42. The overall ESOP cost identified in such a financial year divided over the span of vesting was around RM 710,000.

In another case, a Malaysian manufacturing firm of medium size was interested in implementing performance-vested options to its senior management. Since the vesting was based on the company meeting certain EBITDA objectives in a duration of three years, a conventional Black-Scholes model could not be used. Instead it was modeled by running a Monte Carlo simulation based on thousands of scenarios to describe the probability of hitting each performance threshold. The end result was a lower valuation that the directors had initially foreseen, but more justifiable – and more in line with the expectations of the auditors.

These are examples of what is important: ESOP valuation is not a universal undertaking. The approach, suppositions, and inputs should be adjusted to the particular scheme and company situation. That is why it generally is more judicious to outsource the services of a qualified ESOP valuation services provider of private companies in Malaysia provider instead of trying to do the calculation in-house, especially when the outcome of this procedure will be evaluated by other auditors or investors.

Pitfalls, Lessons, and What Professionals need to Be aware of – ESOP Valuation Firm Malaysia

Despite an effective procedure and competent advisors, there are recurrent difficulties in the ESOP valuation of the Malaysian market. This knowledge in the early stages can save a lot of time and money in the course of valuation engagement and audit.

Table 3: ESOP Valuation Problems and ESOP Valuation Resolutions – ESOP Valuation Firm Malaysia

| Challenge | Why It Happens | Practical Solution |

| No market share price available | Company is unlisted/private | Use DCF or market comparables to derive fair value |

| Estimating volatility | No historical trading data | Use peer-listed company proxy volatility |

| Defining expected option life | Uncertain employee behaviour | Apply simplified method or industry benchmarks |

| Incomplete financial records | Early-stage startup documentation gaps | Work with management accounts and assumptions |

| Regulatory interpretation gaps | Evolving SC / Bursa / MFRS guidance | Engage qualified valuation firm for guidance |

One of the learning that comes up on a regular basis when working with companies on valuing employee stock option plans in Malaysia is that the quality of documentation is usually more consequential than the valuation model itself. It is not even a specific number that auditors and regulators seek but rather a transparent, repeatable and evidence-based process. Those businesses that maintain a comprehensive documentation of their assumptions, sources of data and model inputs will sail through the audit process much easier.

The other similar learning is associated with timing. This is because there are numerous instances of companies hiring a valuation firm after the financial year-end when the audit process is already in progress. It is then that the rush to have figures finalised may result into corners being cut. Best practice is to have a valuation firm involve them prior to, or contemporaneously with, the ESOP grant and so the fair value is determined at the same time as the grant date, which is, in reality what the MFRS 2 is demanding.

Table 4: Quick-Reference Learning Guide : 4 Steps to Professionals – ESOP Valuation Firm Malaysia

| Step | What to Know | Why It Matters | What to Do |

| 1 | Understand ESOP structure | Options vs. shares affect valuation method | Review scheme rules and grant letters early |

| 2 | Know the compliance framework | MFRS 2 requires fair value at grant date | Identify reporting obligations before grant |

| 3 | Choose the right valuation model | Method depends on vesting conditions & data | Consult a qualified valuation firm |

| 4 | Document and disclose properly | Auditors and regulators need clear evidence | Keep records of assumptions and inputs |

Conclusion: Practical Implications to the Profession –ESOP Valuation Firm Malaysia

The ESOP valuation in Malaysia is at the border of finance, law, accounting, and people strategy. To any of the professionals in these fields, it will help you become a better provider of service to the organisations you serve, be it as an employee, adviser, auditor or even as a business owner in the future even by developing even a basic knowledge of the subject.

As an effective point of departure, the following is what you ought to learn out of this paper. First, understand that ESOP valuation requirements and methods in Malaysia are regulated under MFRS 2 and any company that has the share-based compensation is required to comply not only listed firms. Second, the valuation model must be appropriate to the structure of the options you are giving; there are no reasons which make you just use Black-Scholes when your scheme has performance conditions or non-standard features.

Third, when you are dealing with a startup or a private company, be especially sensitive regarding the underlying share value – it is the most disputed input, and the one that is the most likely to be challenged by auditors. Fourth, spend time in documentation. An accurately documented list of assumptions is superior to a well-polished looking figure with no rationale to it. And fifth, engage early. Hiring an expert in ESOP valuation services of a Malaysian company prior to the grant date as opposed to the audit places you in a better position to have a smooth ride.

Malaysian ESOP market is still growing. The need to have transparent, compliant, and supported valuations will continue to increase as more and more private companies and startups are attracted to share-based remuneration to attract and retain talent. Those professionals who know how to compute ESOP valuation in startups in Malaysia, and when to call in the services of the professionals, will be in a good position to make a real value addition in the area. This is not to become an expert in valuation in a matter of days, but to make sure that one is able to grasp the process well enough so that she is able to ask the right questions, deal with the right players and prevent the most typical pitfalls.