How ESOPs Dilute Existing Shareholders

A Practical Guide for Finance Professionals

Why ESOP Dilution Matters to Shareholders

Employee Stock Ownership Plans (ESOPs) are the new mainstay of corporate compensation. They were first widely used by high-tech start-ups in Silicon Valley in the 90s, but have now become commonplace across all business sectors – from early stage enterprises to listed multinational corporations – as a tool for motivating, recruiting, and retaining key employees. The concept is that employees are issued with options or shares in the company, incentivising them to work towards corporate success. But for current shareholders, there is another plot, which is often overlooked until the effects of dilution are felt. Hence, the ways in which ESOPs dilute existing shareholders are not just a theoretical construct, but a commercially important concept for all those engaged in corporate finance, investments, and stock management.

Dilution happens because ESOPs create new shares in the company. Once the options are exercised and converted into shares, the relative shareholdings of all existing shareholders will fall, despite the fact that the number of shares they hold has not changed. An entrepreneur who once held 40% of a company’s shares could have their ownership percentage reduced to 33% after a few vesting cycles – not because they sold a share, but simply because the total number of shares increased. This is the subtle, behind-the-scenes reality of ESOP dilution, and can surprise those without experience in equity mechanics.

In this article, we look at how ESOP dilution works, the effect of ESOP dilution on existing shareholders, how companies structure and manage their share pool, and how the lessons from real-life examples can inform professionals. Whether you are a junior analyst working to understand a cap table, an early- to mid-career manager and just receiving your first grant of options, or even an employee considering a position that comes with an equity component, understanding shareholder dilution from ESOPs will help you make more informed decisions and ask better questions.

Understanding the Mechanics of ESOP Dilution

Let’s take a hypothetical example to explain dilution. Let’s take a private tech company – Verano Technologies, for example – that was originally established with 10 million shares owned by three co-founders. Each co-founder has approximately 3.33 million shares, or a third of the company. Until an ESOP is created, all significant decisions and dollars of future value are shared equally by the three owners.

But now, if Verano establishes an ESOP of 2 million shares, or 20% of the fully diluted share count (10 million shares now outstanding plus 2 million new ones make 12 million shares total), then each founder’s interest has been reduced from 33.3% to 27.8%. Now each founder’s interest in the company is immediately reduced from 33.3% to 27.8%, despite the fact that he or she hasn’t sold, gifted, or given away a share. Suppose Verano later engages in another hiring spree and increases the ESOP pool (say by 1.5 million shares). The fully diluted million now is 13.5 million shares, and the founder’s share drops to 24.7%. This is the most basic way ESOPs dilute existing shareholders: each time you increase the size of the pool, you decrease shareholders’ relative stake in the company.

There are two forms of dilution. Authorised but unissued dilution is when the ESOP pool is established, and shares reserved – the denominator of the capitalisation table increases before options have been exercised. Exercised dilution is the next step, when vested options are exercised, and the assumptions of the ESOP are realised by converting the options into shares, at an exercise price equal to or close to the fair market value at the time the options were granted. These are both important from a shareholder perspective, but it is the former – the reservation of shares – that impacts the immediate landscape of a funding round or valuation exercise.

Table 1: Founder Ownership Impact from ESOP Pool Expansion

| Stage | Total Shares | Founder A Shares | Founder A % | ESOP Pool % |

|---|---|---|---|---|

| At founding | 10,000,000 | 3,333,333 | 33.3% | 0% |

| Post ESOP creation (2M shares) | 12,000,000 | 3,333,333 | 27.8% | 16.7% |

| Post ESOP expansion (+1.5M shares) | 13,500,000 | 3,333,333 | 24.7% | 25.9% |

| Post exercise of 2M options | 13,500,000 | 3,333,333 | 24.7% | 11.1%* |

*Remaining unexercised options still reserved; exercised options are now held by employees as shares.

Five Core Principles of ESOP Shareholder Dilution

Those who are involved in equity discussions – as employees, in the board room, in investment discussions – benefit from understanding the mechanics of ESOP dilution. The essentials are outlined below in five points.

- The pool dance affects pre-money value. As part of their investment negotiations, venture capitalists tend to insist that the ESOP pool be established or increased prior to the investment. So the pool’s dilution impact is fully offset by the founders and existing shareholders, rather than the new investors. A $10 million dollar pre-money valuation with a 20% pool already established is not the same as a $10 million dollar pre-money valuation with the pool to be set up after the investment – in the latter case, the founders get less for their shares.

- Dilution happens over time. The most common vesting schedule is four years, with the first 12 months as a “cliff”, after which employees will gain 1/12 or 1/3 of the shares each month or quarter, respectively. This spreads the dilution, allowing the company to plan for the cap table without a sudden increase in the total number of shares.

- It depends on the exercise price and fair market value. Options are usually granted at the fair market value of the share at the time of the option grant. In the case of start-ups, this is often determined by an independent valuation (a 409A valuation in the US, or similar). If the value of the company increases significantly after the options are granted, then the difference between the exercise price and the market price becomes real economic value to the employees (and diluted value for other shareholders).

- Anti-dilution helps, but not enough. Certain preferred shareholders are able to include anti-dilution provisions in their investment contracts. These (especially full ratchet or weighted average provisions) increase the conversion ratio of their preferred shares to address the impact of new share creation, including ESOP growth. But, unlike preferred shareholders, rank-and-file employees and early retail shareholders of public companies do not typically enjoy these rights.

- Unvested options still count towards fully diluted. When calculating a company’s valuation multiples, such as price-earnings or price-to-sales, or earnings per share, financial analysts should use the fully diluted share count, which takes into account all outstanding options, warrants, and other convertible securities – even unexercised ones. Failing to do so results in inflated per-share figures and incorrect analysis.

Table 2: Key Drivers of ESOP Dilution and Shareholder Impact

| Dilution Driver | Who Is Most Affected | Degree of Impact | Protective Mechanism |

|---|---|---|---|

| ESOP creation (pre-funding) | Founders, early shareholders | High | Cap table modelling, negotiation |

| Option exercise post-vesting | All existing shareholders | Moderate | Buyback programmes |

| ESOP pool growth (development) | Series A/B shareholders, founders | Moderate–High | Anti-dilution provisions |

| Secondary option grants (retention) | All common shareholders | Moderate | Refresh grant limits |

| Early vesting (M&A event) | Acquirer, existing shareholders | Variable | Double-trigger clauses |

Real-World Examples of ESOP Dilution Management

Putting it into practise. How ESOP dilution affects existing shareholders is best shown by considering the way companies manage their equity plans.

Take, for instance, an Australian fintech company – typical of many high-tech growth companies in the Asia-Pacific region – that has raised funds from seed to Series B in the past four years. At seed, the cap table was owned by the founders and angel investors. As the firm grew and began to expand its workforce, the ESOP pool was doubled first to 10% of the total share capital, and then to 18%. By the closing of the Series B, the shareholdings of the founding team had declined from 70% to 41% – equally the result of both dilution and ESOP growth. Although each individual founder’s shares were now worth far more (the company’s value had increased by a factor of 10), the shareholders’ proportionate voting and economic rights had been eroded. This is a textbook case of economically sensible, but structurally significant dilution.

A different example is the well-known US public company case. A large technology company with a large outstanding ESOP programme found that its GAAP earnings per share (EPS) were significantly lower than its non-GAAP EPS, simply because GAAP accounting calls for the expensing of stock-based compensation. Wall Street analysts who only tracked non-GAAP measures of profitability overestimated the firm’s profitability relative to shareholder returns. Subsequently, the firm went through a slowdown and cut back on its option grants, with the result that the GAAP-non-GAAP difference decreased, and investors who had been basing their models on the wrong information were surprised. The lesson: shareholder dilution from ESOPs is about knowledge of how equity compensation impacts the financial statements as well as the capitalisation table.

A third interesting example is the use of performance-vesting ESOPs at a European consumer goods firm that sought to link equity compensation to long-term value for shareholders. The board decided not to issue options that only vested on time, but instead a programme where 50% of the equity award vested on tenure and 50% vested if the company’s total shareholder return was greater than a peer index over a three-year period. This helped minimise the dilution risk of poorly performing ESOP grants while still giving management incentives – an approach now taken by many listed companies around the world.

Managing ESOP Dilution in Practice

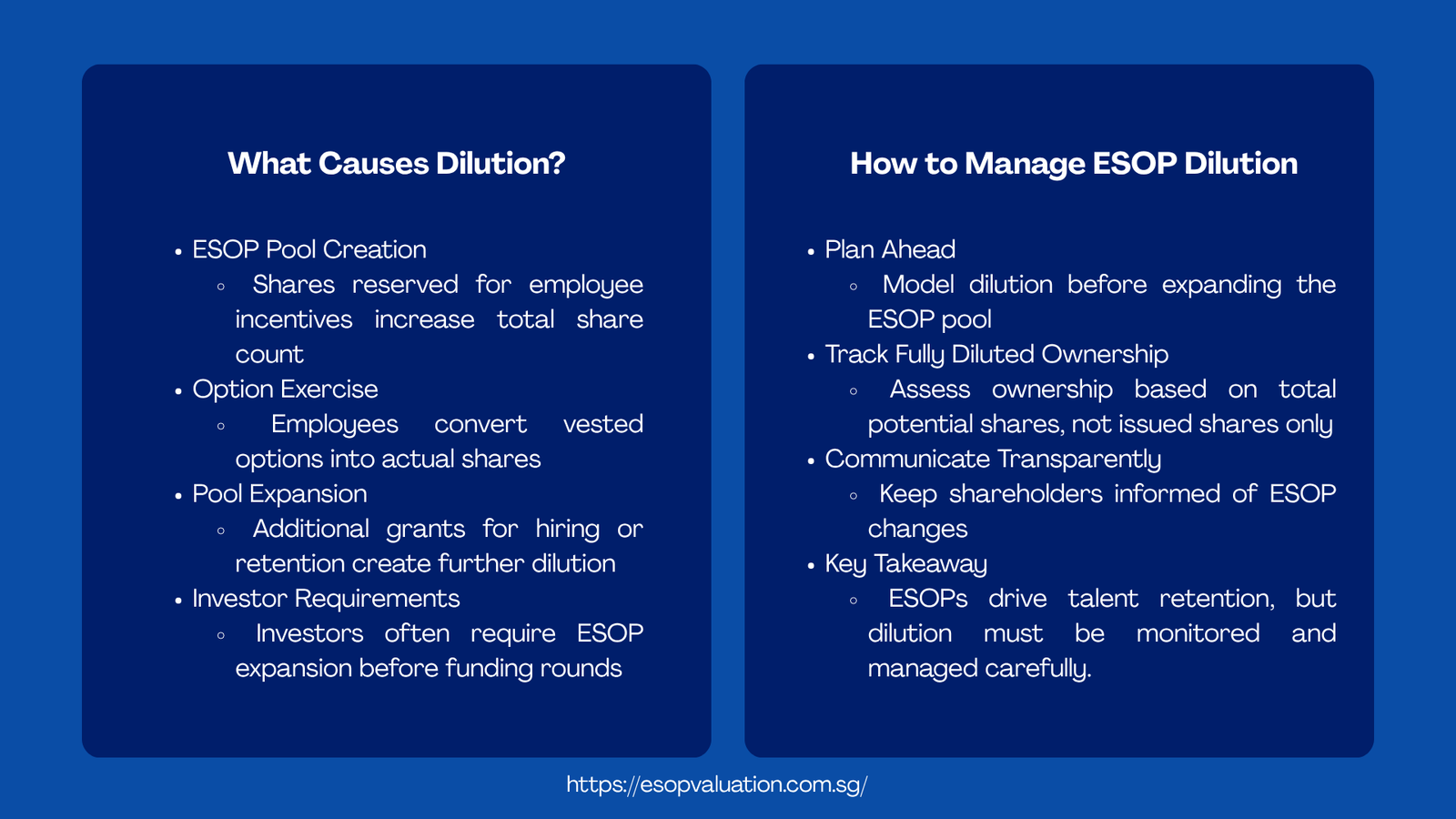

Resolving ESOP dilution is often not a straightforward affair. Broadly, companies are caught between the need to offer competitive equity packages to recruit and retain staff, the aspirations of current shareholders to “keep the pie the same size”, regulatory considerations regarding the pricing and disclosure of options, and the practical considerations of managing grants across multiple jurisdictions.

A common issue is the push and pull between short-term and long-term. Too often, the founders and early CFOs miscalculate the impact of multiple rounds of ESOP over a 5-10 year period. They award options in the early days when the value of the company shares is low, and the pain of giving away equity is not so great. By the time the business becomes profitable or is ready for an initial public offering (IPO), the fully diluted share capital may be far in excess of expectations. This is often an issue for investment bankers and advisors during the IPO process, where the cap table must be “cleaned” (often via option buy-backs, option exchanges, or accelerated exercises) in time to prepare the prospectus.

Another process challenge is the HR, finance and legal coordination. ESOP administration involves tracking options grants, their exercise prices, and vesting schedules, and employee terminations. When employees terminate (either voluntarily or involuntarily), the unvested options generally expire and go back to the ESOP pool, and the vested but unexercised options may have a short exercise period (e.g. 90 days for post-termination exercise). It’s a complex administrative task to keep up with all of these dynamics in a rapidly growing company, particularly in an international company. Mistakes in option accounting and tracking can result in disputes, restatements and regulatory issues.

The lack of information is also a problem for shareholders. In the private sector, minority shareholders may not be provided with regular communication on the size of the ESOP pool, options granted, or the fully diluted share count. This information gap ensures not all shareholders understand the full effect ESOP dilution will have on existing shareholders until it is made public during a material transaction such as a financing round, secondary sale, or merger. Investor rights agreements and information rights clauses are designed to resolve this issue, but are only as good as the shareholders who secure them.

Table 3: ESOP Administration Challenges and Mitigation Strategies

| Challenge | Root Cause | Recommended Mitigation |

|---|---|---|

| Over-dilution at IPO | Excessive early-stage grants | Scenarios of dilution from start; pool size cap |

| Private cos (cap table) | Infrequent shareholder updates | Distribute the quarterly cap table |

| GAAP vs non-GAAP confusion | Stock comp expensing | Train analysts; include both metrics with reconciliation |

| Employee departure tracking | Poor HR–finance integration | Set up equity management system (e.g., Carta, Pulley) |

| Cross-border tax complexity | Multi-jurisdiction grants | Hire global, country-specific equity tax lawyers |

Key Lessons for Shareholders, Employees, and Executives

After decades of experience with ESOPs in thousands of companies, we now have a fairly clear list of lessons. These are not theoretical lessons, but practical lessons that can be used by all practitioners.

For existing shareholders, whether founders, early investors, or employees who were granted equity in an earlier round, the most important lesson is to always think about your shareholding on a fully diluted basis (all shares issued and options outstanding) rather than the current number of issued shares. Shareholders often mistake the amount of their shareholding and calculate their percentage ownership based on the number of issued shares, and then are surprised to find their percentage ownership is lower when viewed on a fully diluted basis. If you are a shareholder in a private company, make sure to obtain the fully diluted capitalisation table, including all authorised but unissued options, the next time you look at your shareholding. It will be free and may alter your view on the deal.

For those receiving stock option grants (ESOPs), make sure you understand your grant before you put a dollar value on it. Understand the vesting schedule, the exercise price, the company’s last 409A (or equivalent) valuation, as well as the circumstances under which your options will be forfeited if you resign or are fired, or if the company is bought out. This information is contained in your option agreement and equity plan documents, and while the legal speak can be hard to digest, the financial consequences are not. The difference between being acquired above or below your exercise price, or between having a single vs. double trigger acceleration provision, can mean the difference between making a substantial gain and walking away with nothing. The first step to understanding shareholder dilution from ESOPs is to read the fine print on your own share grants.

The take-away for corporate leaders and boards is planning and disclosure. Equity is a currency and, like all currencies, can be inflated. The companies that get this right will have disciplined approaches to their ESOP pools, setting these at the right size (relative to their competitors), refreshing the pool in sensible ways (rather than in response to events), and communicating these changes in a transparent way to all shareholders. The companies that fail to do so often face difficult battles when it comes to critical times such as raising capital, being acquired, or going public.

Final Takeaways on ESOP Dilution Strategy

ESOPs are, in and of themselves, a valuable and worthy means of creating cultures of ownership and providing incentives. Any dilution resulting from them is not, in and of itself, a bad thing – in most circumstances, it is a reasonable cost-benefit analysis between the cost of the equity compensation and the benefit of having motivated, incentivised employees. The issue is when dilution isn’t fully understood, modelled, or communicated.

For early and mid-career professionals working in corporate finance, strategy, and HR, it is increasingly a core skill to be able to interpret a cap table, understand how option grants work, and explain how ESOPs dilute the existing shareholders. With the growing trend of equity compensation and stock-based investing in companies of all sizes and not just those in the technology industry, these skills translate.

Here are five things you can take away:

- Always ask for and scrutinise the fully diluted cap table, and not only the number of issued shares, when considering an equity position or investment.

- Factor in expected future growth of the ESOP pool before participating in a funding round or receiving an equity grant – dilution is a snowball effect, and the long term is often very different from the short term.

- If you’re an existing equity holder in a private company, insist on data rights to receive periodic information on the fully diluted share count and significant changes to the ESOP pool.

- Fully grasp the difference between “GAAP” and “non-GAAP” earnings in any private company that issues large quantities of equity compensation – the difference represents the economic impact of the dilution and should not be regarded as a minor nuance.

- If you are an employee who receives an ESOP grant, make sure you read the option agreement carefully, understand how options can be exercised, and the deadlines, and seek independent advice before you exercise your options, particularly before a corporate sale.

ESOP dilution and its effect on existing shareholders is worth a study. Those who take the time to study it – not just the underlying concepts, but specifically in relation to the companies they work for, invest in, or advise – will make superior investment and business decisions to those who do not. In an era in which equity compensation is rising in importance as a means of creating and sharing value, this is a real advantage.