Top ESOP Benefits for Companies in 2026

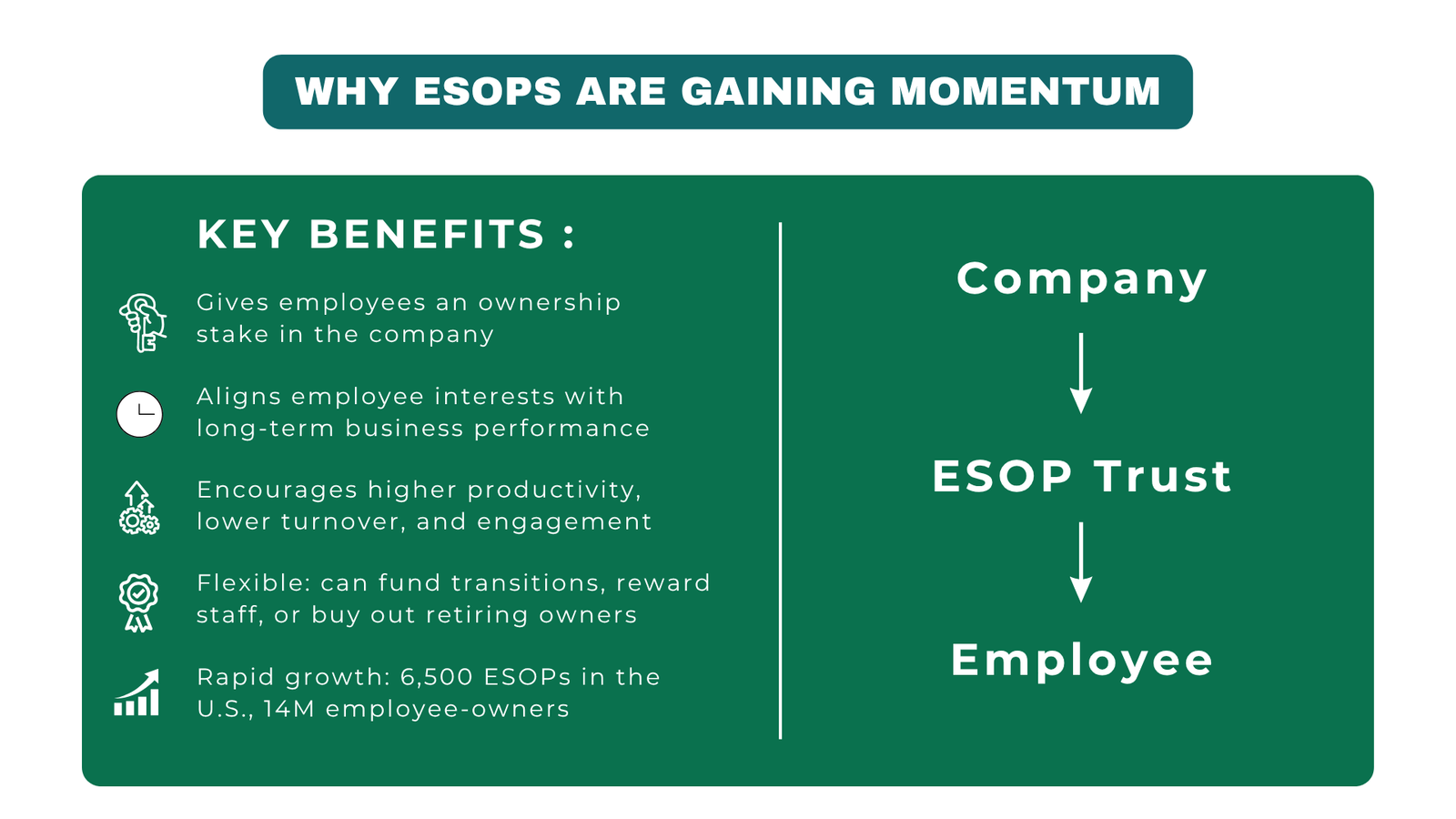

Picture 1 : Why ESOPs are Gaining Momentum

In the world where retention of talents and the engagement of employees are considered as vital as revenue growth, firms are now resorting to creative compensation models to remain afloat. The Employee Stock Ownership Plan, often referred to as ESOP is one of the most potent instruments the modern world has. Although the concept is not new, the suitability of ESOP benefits for companies has become significantly more pertinent over the past few years, particularly with organizations increasingly under pressure to shape the interests of the employees with the long-term organizational performance.

An ESOP is a form of employee benefit plan which provides employees with ownership interest in the company they are employed. As opposed to just getting a salary, participating employees gradually become part-owner, who can enjoy financial prosperity of the company over time. To businesses, this would provide an automatic motivation to work harder, reduce turnover, and have a more motivated workforce without necessarily making any instant cash investments in most buildings.

This paper discusses the major ESOP advantages that the companies will have in 2026, taking one through the working mechanisms of these plans, the operations of the plans, the real-life examples, and what learning organizations can learn about the plans adopted by other organizations successfully. This guide provides pragmatic, well-grounded advice whether you are a junior professional who is attempting to figure out your personal ESOP package, or a manager who is attempting to define the compensation strategy at your own company.

How ESOPs Work and Why Companies Are Adopting Them

An ESOP is an investment based retirement plan that is mainly invested in the stock of its employer. The company establishes a trust, which buys shares on behalf of staff. These are distributed to personal accounts of employees; most of them are distributed according to salary or years of service and are also vested with time. Upon the departure or retirement of an employee they are given the worth of their vested shares in cash form.

Use of ESOPs has especially been prominent within middle sized companies that are privately owned. The National Center of Employee ownership estimates that in the United States alone, there are some 6,500 operating ESOPs with over 14 million employee-owners. This expansion is fueled by several areas: founders aiming to have an effective exit strategy on tax grounds, HRs having retention problems, and leaderships aiming to create a more sustainable company culture.

To the employees, ESOPs are an aspect of deferred savings of wealth – an advantage that increases with the company. To employers, the structure is flexible: it can be employed to finance a business transition, purchase out a retiring business owner or even the incentivize long-term employees. This dual value proposition is the initial key to understanding why ESOP benefits for companies become more and more relevant in the 2020s.

Table 1: ESOP vs. Other Common Employee Benefit Structures

| Benefit Type | Ownership Stake | Tax Advantage | Best For |

| ESOP | Yes — company stock | Significant (company and employee) | Moving between mid-size and large firms. |

| 401(k) Match | No | Moderate | Broad workforce savings |

| Phantom Stock | No (cash equivalent) | Limited | Firms of private groups which are not diluted. |

| Stock Options | Potential (on exercise) | Moderate to high | Startups, high-growth firms |

| Profit Sharing | No | Moderate | Cyclical revenue business. |

Source: National Center for Employee Ownership (NCEO), 2025 data.

The Five Key Steps to Implementing an ESOP Successfully

The establishment of an ESOP is not a decision that can be made over a night. It involves planning and legal structuring as well as financial due diligence. Companies that are planning to take this path need to know the processes involved in order to make expensive errors. There are five major steps that an ESOP commonly uses to implement an ESOP in firms and they are as follows.

Process Flow 1: Step by Step of ESOP Implementation

| Step | Activity | Key Participants | Typical Timeline |

| 1 | Feasibility Assessment – Determine whether an ESOP is a financially and strategically sound idea to the company. | CEO, CFO, Board | 4–6 weeks |

| 2 | ESOP Fair Market Value Assessment — Use an independent to establish the fair market value of the company. | Legal Team, Independent Appraiser. | 6–10 weeks |

| 3 | Plan Design and Legal Structuring Prepare the ESOP plan document, trust deed and financing agreements. | Plan Administrator ERISA Attorney. | 8–12 weeks |

| 4 | Financing & Share Acquisition Fact Sheet: Obtaining financing (bank loan or seller note) and handing over shares to the ESOP trust. | Bank/Lender, Trustee, CFO | 4–8 weeks |

| 5 | Employee Communication and Rollout- Train employees on the working of the plan, the schedule of vesting, and valuation. | HR, Communications Team | Ongoing |

Step two: the ESOP fair market value assessment is the stage that, perhaps, is the most important one. This is the place whereby a qualified business appraiser, who is independent should find out the worth of the company. The valuation directly determines the number of shares that will be issued, the price at which the employees will be issued with equity and the price at which the company will pay in case the shares are repurchased. This is not only a good practice; it is a legal issue under the rules of ERISA (Employee Retirement Income Security Act) in several jurisdictions such as the United States.

The process is progressive in nature. These companies that hasten in the process of feasibility or valuation run into trouble in the future, not only due to challenges in determining share valuation, but also regarding regulatory fines. The most effective ESOP projects do not focus on the process as a one-time-only transaction. Constant communication with employees is especially in this case, as it transforms what might seem as an impalible financial tool into a living and breathing ownership interest.

Real-World Examples and the Lessons They Teach

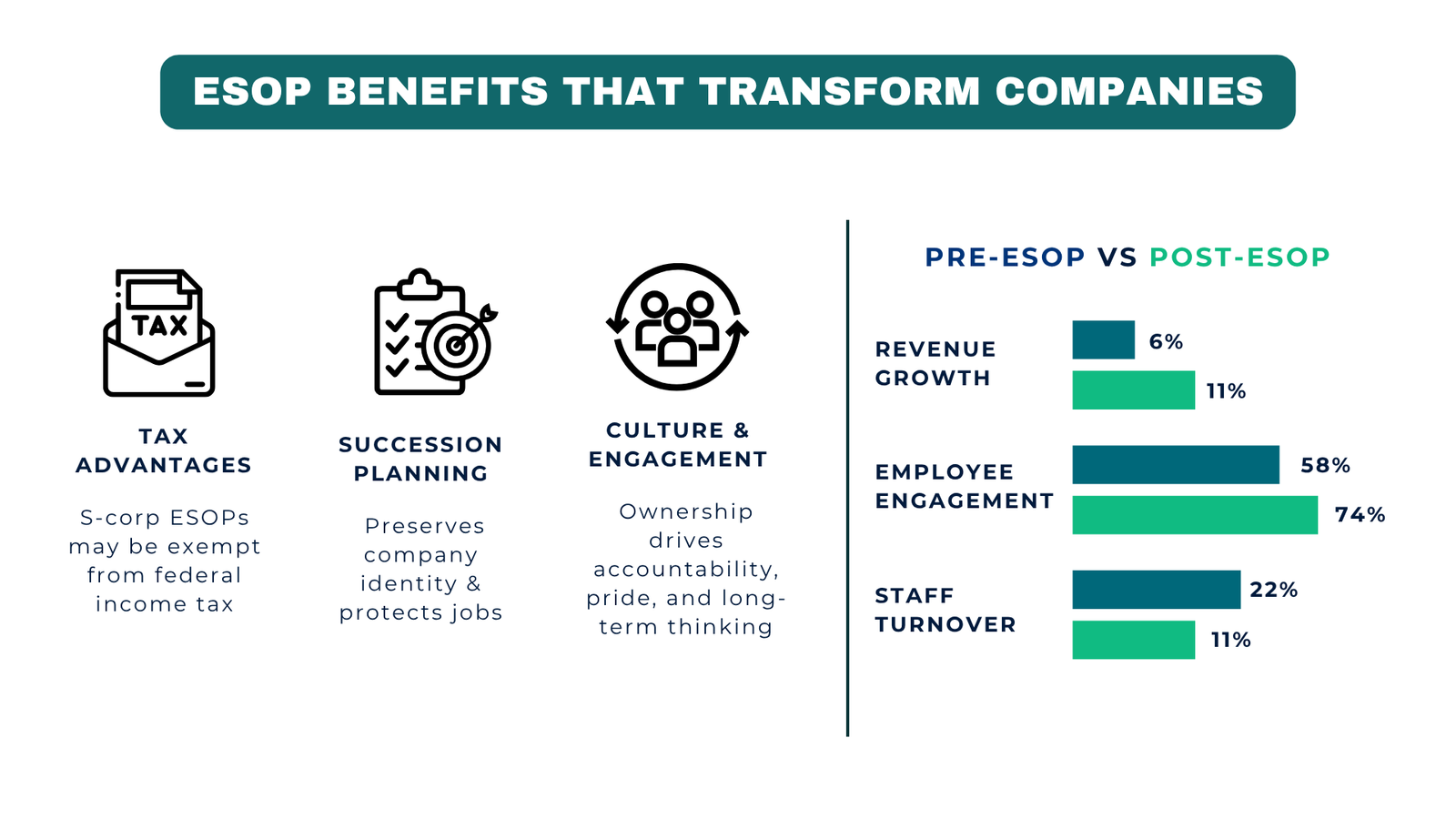

Picture 2 : ESOP Benefit that Transform Companies

One of the quickest ways to appreciate the practical aspects of the ESOPs is to learn by example, i.e. organizations that have already undertaken this route. The trend is similar across the industries and geographies: where the companies employ the ESOPs with a clear understanding, the dynamics of the performance, culture, and the duration of the company are likely to be positively affected.

The example is of a mid-sized U.S.-based engineering company, Hanlon and Associates. The founder of the company, who was almost retiring, preferred to exit the company using ESOP as opposed to selling to a private equity company. The founder was enabled to defer capital gains taxes under the Section 1042 of the U.S.Internal Revenue Code allowing the company to be intact with jobs and company culture preserved by fully transferring 100 percent ownership to the employees over a period of five years. The productivity of the employees who could be measured by the revenue generated per employee increased by 18 percent over the three years after the formation of the ESOP. The moral of this story is that employees would tend to do more than is required of them when they know that their effort directly raises the value of their stocks.

The other example is that of Briarfield Foods that is a family owned food manufacturing company located in the United Kingdom. To finance a management buyout, the company adopted a partial ESOP whereby it retained only 30% of the employee ownership but left the remaining to external investors. What they had found was that what had been done through the annual ESOP fair market value assessment was a tool of strategic planning in itself. The valuation of every year compelled the management to have a truthful discussion on business performance, asset quality, and growth outlooks – which instilled a sense of discipline that was not developed before. The moral here is that the appraisal process is not a form of bureaucratic burden but a good reflection of the actual financial position of the company.

Table 2: Company Performance Before and After ESOP Implementation

| Metric | Pre-ESOP Average | Post-ESOP Average (3 Years) | Change |

| Annual Staff Turnover | 22% | 11% | −11 percentage points |

| Revenue Growth (YoY) | 6% | 11% | +5 percentage points |

| Employee Engagement Score | 58/100 | 74/100 | +16 points |

| Absenteeism Rate | 5.1% | 3.2% | −1.9 percentage points |

| Net Promoter Score (internal) | 32 | 61 | +29 points |

Source: NCEO 2024 Employee Ownership Report; Rutgers School of Management and Labor Relations ESOP Study.

Challenges Companies Face and How to Navigate Them

There are no benefits structure that is devoid of complications and the ESOPs are not an exception. Even though the ESOP benefits for companies are substantial, firms must expect a unique set of problems – not only the administrative burdens of managing the plan on a regular basis but also the economic costs of the repurchase requirement.

Although the repurchase liability is one of the most often underestimated issues. Upon the retirement or departure of the employees, the ESOP trustee is normally required to repurchase their vested shares at reasonable market value. This may have been a huge recurring outlay of cash in the case of companies that have expanded in size. An ESOP workforce that is maturing rapidly can cause a liquidity strain at the worst moment without proper financial forecasting and reserve planning. Other companies such as Meridian Building Products, a hypothetical amalgamation of a number of actual U.S. construction companies, have claimed that they have been forced to reorganize financing arrangements when retirement waves come into their ESOP plans at the same time. The lesson: project the repurchase commitment at the beginning and review the estimates every year.

The other problem is how to ensure the integrity and timeliness of the ESOP fair market value assessment. Appraisals should be done on the basis of annual appraisals by a qualified independent appraiser, not by the accountant of the company or any related party. In case the Department of Labor (or other regulatory body) finds out that the valuation was overstated it can lead to the disqualification of the plans, retroactive tax payable and penalties. The firms are expected to select appraisers who possess special ESOP valuation qualifications, which include the Accredited Senior Appraiser (ASA) designation and report the procedure in detail. Employee trust is also increased with transparency in valuation: employees are more likely to trust that the ESOP is fair (when they know the way their shares are valued).

Process Flow 2: Annual ESOP Valuation and Compliance Cycle

| Month | Activity | Responsible Party | Output |

| Jan–Feb | Prepare and prepare financial statement of valuation period. | CFO / Finance Team | Audited financials |

| Mar–Apr | Hire outside appraiser; perform ESOP fair market value evaluation. | Appraiser, Trustee | Draft valuation report |

| May | Reviews and approves valuation; adequate legal review. | Trustee, ERISA Attorney | Final valuation report |

| Jun–Jul | Update account statements of participants on new share price. | Plan Administrator | Employee statements |

| Aug–Sep | Form 5500 (annual plan report) to the IRS/DOL. | Plan Administrator, CPA | Regulatory filing |

| Oct–Dec | Revised the projections of repurchase obligation; annual plan. | CFO, Plan Administrator | Repurchase forecast |

The third challenge that many small companies are not aware of is administrative burden. Complex federal regulations (under the ERISA in the U.S.) that demand plan administrators who are specialized, plan annual audits (with more than 100 participants), and frequent trustee supervision govern ESOPs. Those companies who fail to budget well on these expenses, which may be as low as 20,000 to more than 100,000 per annum based on the size of plans, usually see the administrative tail pull the strategic dog. The pragmatical approach is to engage an experienced ESOP third party administrator (TPA) at the very beginning and factor in the compliance costs in the business case prior to implementation.

Long-Term Strategic Value: Tax Advantages, Succession, and Culture

In addition to the mechanics of operation, the more strategic argument in support of ESOPs lies on three pillars: tax efficiency, succession planning and organizational culture. All of these support each other, and when combined, they lead to the reason why the ESOP benefits for companies are becoming a part of the discussion at the boardroom, and not just within the HR department.

Tax wise, ESOPs have one of the most attractive incentives in the corporate benefit arena. In the S-corporation ESOPs (especially popular in the United States), the equity percentage of the ESOP is not subject to federal – and commonly state -income taxation. One hundred percent S-corp ESOP does not pay any federal corporate income tax at all, and the result is that there will be increased funds to reinvest in growth, debt repayment, or contribution to employee accounts. In the case of C-corporations, capital gains tax is deferred by the selling shareholders under the IRC Section 1042 to sell to ESOP and invest in qualified replacement property. These are not fringes savings – they may go up to millions of dollars in mid-sized companies.

On the succession front ESOPs provide an alternative third way of selling the business to another company and passing it on to family which is not always quite available and may not always be desirable. In the case of a founders that have developed a business over several decades, an ESOP sale will maintain the identity of the company, safeguard employee jobs, and enable the exiting owner to take exit at the fair market value (determined as required by the ESOP fair market value assessment). It is a change that respects financial and human heritage of the business. Culturally, the concept of employee ownership also changes the psychological bond between the workers and the organization. Studies have demonstrated again and again that ESOP organizations do better in such measures as productivity and profitability, or innovation and safety history, not necessarily due to their monetary incentive programs, but due to the fact that ownership instills accountability, pride, and a long-term orientation which cannot be fully simulated by a program of annual bonuses.

Conclusion: Actionable Insights for 2026 and Beyond

The argument of ESOPs in 2026 is strong in various aspects. An ESOP is a solution of a kind to companies looking to maintain the highest quality talent, develop a robust culture, have a leadership succession plan, or in a major tax benefit. ESOP company benefits are not abstract concepts- they have been supported over decades of performance statistics as well as actual case experiences across business sectors and locations.

Five actionable insights that you can implement to move forward with an ESOP are the following, in case you are a professional working at a company that is considering an ESOP:

- Start with the numbers. Carry out initial feasibility study and then commit. Know valuation of the company, predicted share price growth and repurchase obligation.

- Give emphasis to the valuation process. The ESOP fair market value estimation is not a trifle. Engage a qualified and separate appraiser and get the valuation as an annual strategic check.

- Be open and communicate with employees. It is only the ownership that is motivating when it is understood. It is essential to regularly update on the share value, the progress of the vesting and the performance of the company.

- Plan for the long tail. Bond the repurchase investment during 10 to 15 years. Establish reserves and review your assumptions each year as the workforce is growing older and the vesting timeline is shortening.

- Early involvement of specialist advisors. ESOP implementation will involve the coordination of the ERISA attorneys, independent trustees, third-party administrators and qualified appraisers. One of the most frequent but expensive errors that companies commit is attempting to reduce the expense by employing generalist advisors.

Those organizations that will do well in the coming years will be the ones that consider their people not only as employees, but as stakeholders who are interested in the outcome. One of the most direct and proven methods of realizing that principle is in the form of an ESOP. The payoffs, financial, cultural and strategic, are huge and long-lasting to those companies that have the time and resources to do it right. The ESOP benefits to companies do not merely represent a line entry on a benefits brochure; they represent a substantial rethinking of the concept of what it takes to create a business that lives.