IFRS 2 Accounting for Employee Stock Options

Picture 1 : Introduction to IFRS 2

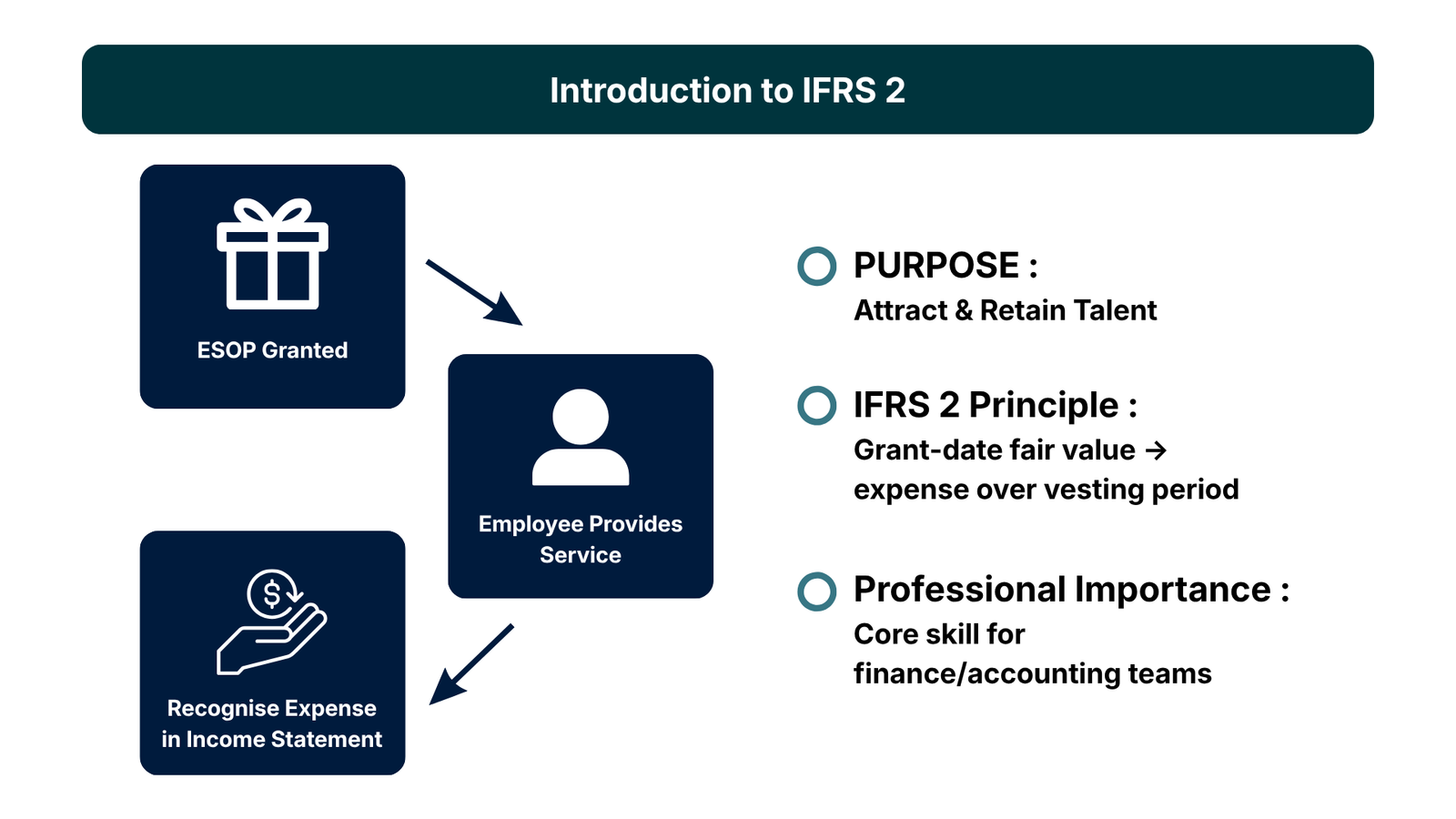

Stock options awarded to employees have been among the most popular means of attracting, retaining, and motivating talent especially in fast growing industries where cash compensation might not be the only tool to help compete with skilled employees. However, there is one important accounting requirement behind any stock option grant. According to International Financial Reporting Standards, IFRS 2, officially known as Share-based Payment, is the standard that regulates the recognition and measurement of the cost of the share-based compensation by companies. As a professional in the field of finance employed in a company that offers IFRS 2 stock options, this standard is not an optional requirement of the profession it is one of the essential professional standards.

The basic idea of IFRS 2 is simple, where an employee is given a stock option as a part of his compensation, then the company is being given a service and the fair value of that service should be charged as an expense in the income statement over the period in which the service is received. As a matter of fact, however, there is much complexity in applying this principle in practice. The determination of fair value, choice of a proper valuation model, administering of vesting terms, processing of modifications and cancellations, and proper employee stock option administration records – all of these are activities that demand both technical expertise and professional judgment.

In this article, the authors give a practical analysis of IFRS 2 in its application concerning employee stock options. It is authored to the juniors and middle level finance and accounting practitioners and those who are about to take up positions in financial reporting, compensation structuring and transaction advisory. The article discusses the accounting process, the accounting difficulties of ESOP fair market value determination, the pitfalls to avoid based on the real life examples, and what best practices can do to enhance your approach to IFRS 2 stock options in any organisational environment.

The Core Accounting Framework Under IFRS 2

Central to this IFRS 2 is that companies need to determine the fair value of equity-settled share-based awards at the time of grant and to recognise that value as an expense throughout the period of the vesting- the period during which an employee is required to render services to be entitled to receiving his or her options. This is also referred to as the service period, or requisite service period. In the income statement, the expense will be accrued in the staff costs or compensation expense, and the balance will be credited to the equity reserves. Notably, the fair value of the grant-date is fixed; the value of the company shares would not increase or decrease the identified expense on equity-settled awards.

The date at which the company and the employee have a mutual understanding of the terms and conditions of the arrangement is considered to be the date of grant date under IFRS 2. This is significant since ESOP fair market value determination has to be carried out as at this date. In the case of listed companies, the share price is seen but the fair value of the option still should be determined, based on a suitable option pricing model to consider those variables, including the exercise price, anticipated term, the volatility of the share price, risk-free interest rates and anticipated dividends. In the case of the unlisted companies, the underlying share price needs to be estimated as well, which is one more complex issue.

Another significant difference between equity-settled and cash-settled share-based payments under IFRS 2 is made. The most frequent type of employee stock options is equity-settled, which are not remeasured and measured at the time of granting. Awards settled in cash like share appreciation rights paid in cash are remeasured at every reporting date until payment, which creates a continuing volatility on the income statement. This difference has some practical implications to the way companies devise their compensation plans, and how finance departments should deal with the current employee stock option administration process.

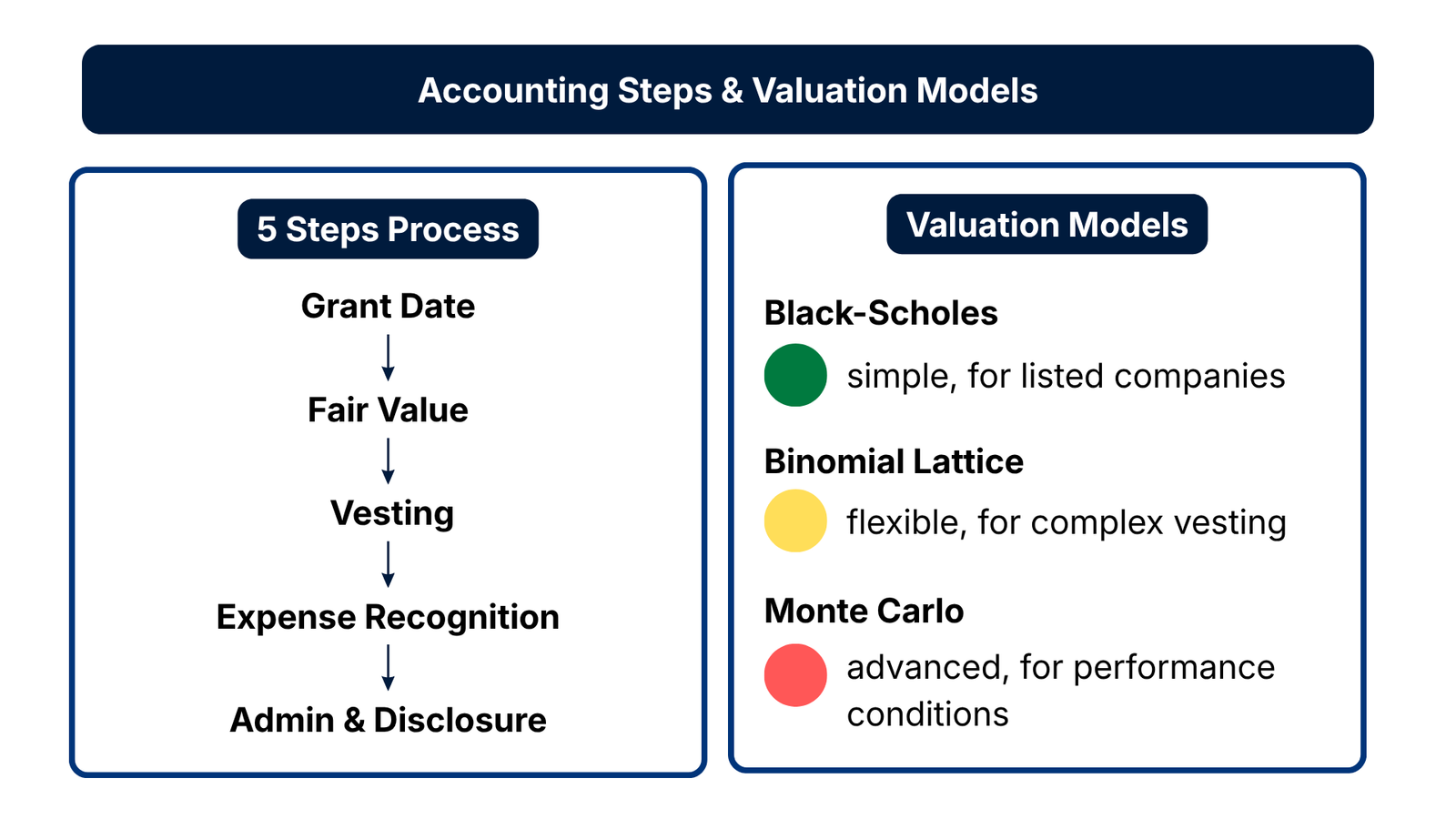

ESOP Fair Market Value Determination: Methods and Inputs

Picture 2 : Accounting Steps & Valuation Model

The most technically challenging part of the accounting of IFRS 2 stock options is the fair value of the options at the grant date. The IFRS 2 does not specify which model of valuation should be used, although it must be consistent with generally accepted methods of values and must include the variables that a knowledgeable and willing market participant would take into account. As practice shows, the Black-Scholes-Merton model and the binomial lattice model are the most popular models, each having its advantages and disadvantages.

The Black-Scholes-Merton model has many applications as it is relatively simple and consistent. It has five basic inputs which include current share price, the exercise price, the expected term of the option, the expected volatility of the share price, the risk-free interest rate and the expected dividend yield. All these inputs are judgmental. Predicted volatility, such as that of in a stock, is usually computed based on historical data on the share price, though with new or untraded companies the implied volatility of similar listed stocks is sometimes used instead. The anticipated period usually falls short of the duration under which the option was contracted since employees will exercise prematurely. ESOP fair market value determination is not just a mathematical formulation that is, it is an auditable well-supported judgement exercise.

Although more complicated to implement, there is the binomial lattice model which is more flexible. It captures the dynamics of the share price through several steps and is therefore better able to accommodate the variable exercise patterns, the market conditions and early exercise assumptions. The Monte Carlo simulation may be used when complex investment plans are required to be used in companies, i.e. performance requirements based on market indices. In either model adopted, the most important principle under IFRS 2 is that any assumptions made are reasonable and in line with the market data as observed where possible and clearly stated. These assumptions will be very closely examined by auditors especially when it comes to unlisted companies where even the share price itself must be estimated.

| Valuation Model | Best Suited For | Key Advantage | Key Limitation |

| Black-Scholes-Merton | Standard options of listed companies. | Easy to audit, simple and widely accepted. | Volatility is assumed to be constant; less flexible at early exercise. |

| Binomial Lattice | Companies with complicated vesting or exercising pattern. | Flexible; models changeable exercise behaviour. | More difficult to construct and report to auditors. |

| Monte Carlo Simulation | Performance conditions that are based on the market (e.g. TSR hurdles) | Precisely represents path-dependent conditions. | Intensive computing; needs limited knowledge. |

Table 1: Comparison of Option Valuation Models Under IFRS 2

In the case of unlisted companies, the ESOP fair market value determination is further complicated by the fact that the fair value of underlying shares should be determined. They are often used as discounted cash flows, earnings multiple values observed against similar-based companies, and the latest transaction prices. The selected strategy must be in line with the stage of development of the company, availability of sound financial forecast as well as the valuation base on other interests like tax planning or fundraising. The audit finding that is frequent is inconsistencies between the valuation basis adopted as IFRS 2 and the basis adopted elsewhere in the business.

Five Key Steps in the IFRS 2 Accounting Process

Employee stock options managed under end-to-end IFRS 2 accounting process have a systematic course of action. To the professionals working in the financial reporting, payroll, or employee stock option administration, it is crucial to comprehend this entire process as a unit other than the valuation component that will exist in isolation of other components to manage schedules, allocate tasks, and prevent mistakes. The following five steps are the basic workflow of equity-settled stock options of employees.

| Step | Phase | Key Activities | Output |

| 1 | Grant Date Identification | Ensure that terms are understood mutually; approve the document board and acceptance of terms by the employees; register grant date formally. | Memorandum of granting date; signed option contracts. |

| 2 | Fair Value Measurement | Choose the right model of valuation; collect and verify all the material input; conduct ESOP fair market value determination; record assumptions. | Model output with sensitivity analysis and assumptions log and model valuation. |

| 3 | Vesting Conditions Evaluation. | Categorize conditions as service, non-market performance or market-based; establish accounting treatment of each one; establish vesting schedule. | Condition classification memo, vesting schedule. |

| 4 | Expenses recognition and journals are the two categories of costs that are recognized and recorded respectively. | Divide fair value by the period of vesting by straight-line or accelerated method, credit to staff costs, and credit to equity reserve per period. | Regular journal entries; schedule of reconciliation of IFRS 2 expense. |

| 5 | Continuing Administration & Disclosure. | Record forfeitures, exercises, modifications and cancellations; calculate accruals of expenses; prepare disclosures of notes in financial statements. | Revised option register; disclosure notes; workpapers that were ready to be taken by the auditors. |

Table 2: Five-Step IFRS 2 Accounting Process for Employee Stock Options

The second and the third steps, which are the grant date identification and fair value measurement, establish the basis of all the steps that follow. Mistakes at this point, like a wrong grant date or one that has poorly supported valuation inputs, carry forward with the whole accounting period and may have to be restated. On step three, which is the assessment of the vesting condition, many of the preparers face conceptual problems. The IFRS 2 identifies a big difference between the service conditions and performance conditions, market and non-market performance conditions, as each is treated differently in calculating the expense.

The grant-date fair value does not record non-market vesting conditions, including the attainment of a revenue goal. Rather, the company makes an estimate of the number of options that are likely to vest and then revises the estimate on that date, and modifies the amount of expense that has cumulated. Conditions market-based, like the total shareholder return hurdle, are factored in to the itself of the grant-date fair value and are never again adjusted, even after the market condition may not ultimately be satisfied. It is one of the counterintuitive features of the IFRS 2 stock options and a common source of misuse.

The fourth and fifth steps – expense recognition and continued employee stock option administration should be disciplined and well-managed in terms of data. The option register should be maintained in accordance with the entry, exit, exercise or grant adjustment of employees. Administrative errors lead to cumulative errors that are hard and time consuming to rectify at the end of a year. Firms with substantial option books, especially those that are about to go public or do a financing round, tend to find that decades of poor record-keeping have left them with substantial restatement risk at a time when good financial reporting is the order of the day.

Challenges, Real Cases, and Lessons Learned

Picture 3 : Challenges & Compliance Best Practices

In spite of the comparative maturity of IFRS 2 (the standard has been in place since 2005), the standard still produces a high amount of audit report, restatements and regulatory commentary. A review of actual practice trends provides valuable guidelines to whoever may be concerned with applying or reviewing this standard.

A common pitfall is that where the companies postpone the formal grant date by not communicating the option terms to the employees as soon as the board has approved them. The IFRS 2 requirements do not allow the grant date to be earlier than the date when workers can mirror a mutual comprehension of the grant conditions. In a number of reported instances where European technology firms were about to issue an initial public offering, the accounting grant date was established as of the board approval date, and the communication was made to employees weeks later. As soon as the discrepancy was detected at grant-date fair values, there was a need to recalculate higher-share-price grant-date fair values with an earlier date, leading to increased recognised expense and for some, restatements in prior years.

A second similar struggle is associated with changes. Where a company reprices options (e.g. lowering the exercise price when shares have fallen in value) IFRS 2 would require that the incremental fair value of the change be recognised as an incremental expense. An example of a software company in North America that had repriced a significant part of its option pool in 2020 due to the pandemic-related declines in share prices, first failed to compute the incremental fair value, and instead of using the incremental approach, it handled the change as a cancellation and re-issuance. This led to an understatement of the compensation expense which was found during the successive audit of the company in the Series C round and had to be corrected before the financing round could be closed. The moral of the story was that change must involve particular and close accounting handling, but not a gut feel or short cut method.

| Common Challenge | Root Cause | Financial Impact | Preventive Measure |

| Incorrect grant date | Lag time between board and communication with employees. | Restatement may; higher fair value. | Communication of document grant date is contemporaneous. |

| Forfeiture rate errors | Inability to revise option register of leavers. | Excessive or insufficient cost statement. | Option register reconciliation to HR records on monthly basis. |

| Modification mistreatment | Repricing which is regarded as cancellation and reissue. | Underreporting compensation cost. | Use IFRS 2 fair value approach at a time. |

| Inappropriate classification of conditions. | Market and non-market conditions in confusion. | Wrong expense reversal of non-vesting. | Write Memo on classification of formal conditions at grant. |

| Disclosure gaps | Inadequacy in disclosure of notes on assumptions. | Audit qualification risk; regulatory comment. | Disclose under IFRS 2 checklist on top of every reporting period. |

Table 3: Common IFRS 2 Challenges, Causes, and Preventive Measures

The third challenge is that especially most of the unlisted companies that grow fast do not have a formal employee stock option administration function. In start-up companies, option grants are frequently managed pastorally in spreadsheets managed by one of the founders or a single member of the finance team. These records are no longer reliable as the option pool increases and turnover among employees takes place. By the time the company finally prepares audited financial statements, be it in the context of a fund raid round, acquisition or IPO, the cost of putting together a full and accurate option register based on partial records can be high. This issue was precisely what was faced by a number of European fintech companies that also were undergoing pre-IPO audits between 2020 and 2023, where some companies found grants that had never been written down and others found discrepancies between the legal contract and accounting entries.

Building a Robust IFRS 2 Compliance Process

Compliance under IFRS 2 of stock options is not a one-time event to organisations that are serious about the process of making sure they get everything right, this is an ongoing process that entails plan design, grant execution, periodic reporting and the preparation of an audit. Creating an effective compliance process must be well-owned, have systems in place, and be well-documented. The process flow shown below shows how a well-planned finance team can deal with the annual process of compliance with IFRS 2.

| Step | Phase | Key Activities | Output |

| 1 | Plan Design Review | Check IFRS 2 compliance of ESOP plan rules; make sure that the terms of vesting are stated clearly; liaise with legal and tax counsel. | Legal and tax sign-off Compliant plan document. |

| 2 | Grant Cycle Management | Write grant letters/ record date of grant; have employees sign; update option register immediately. | Signed grant agreements; revised option register containing grant date and terms. |

| 3 | Annual Valuation Update | Hire valuation specialist or do internal model; reconcile inputs to market information; record ESOP fair market value determination. | Valuation report; file of assumptions support; previous comparison to a year. |

| 4 | Journals and Expenses Calculation. | Run IFRS 2 expense schedule; make updates to actual forfeitures and new grants; make post period-end journal entries; reconcile to prior period. | IFRS 2 expense schedule; journal entries signed-off; commentary on variance. |

| 5 | Preparation of Disclosure and Audit. | Preparation of note disclosures according to IFRS 2 para. 44-52; put audit working papers pack together; answer auditor questions. | Disclosure of audited notes; terminated audit inquiries; clean signing-off of audit. |

Table 4: Annual IFRS 2 Compliance Process Flow

A committed employee stock option administration system or module is one of the largest investments that can be made by a finance team. Although spreadsheet based tracking works well with small option pools it rapidly becomes prone to error as the pool of optionholders, grant tranches and any sort of vesting take effect. Equity administration systems specifically created to support any of the above, e.g. those of various providers around the world, will automate the grant register, vesting computations and IFRS 2 expense schedules, so much more effective at minimizing the risk of manual error and enhancing audit preparedness. This is an investment that should be made at the earliest by companies that are close to their initial external audit or a pre-IPO audit.

The other pillar of a good compliance process is documentation. Any premise that is relied upon in the ESOP fair market value determination must be evidenced, whether it is the past price of the shares, the analysis of other companies, or a management story as to why a certain anticipated term was applied. The assumption logs, model output and sensitivity analysis should be stored as permanent working papers. Poor disclosed IFRS 2 in a regulatory setting where securities regulatory agencies are subject to scrutinizing financial reports, as in the case in the United States, United Kingdom, and throughout the European Union, are a common cause of comment letters and restatements requests.

Last but not least, cross-functional coordination is necessary. The finance department is not capable of dealing with the IFRS 2 stock options in isolation. Legal departments will be required to present signed grant papers. Human resources should report leavers, promotions, and the change in employment status to the finance regarding the vesting issue. The tax treatment of option exercises should be made known in payroll teams. And senior management has to be aware of the income statement implication of proposed option grants prior to approval. ISFRS 2 errors and disclosure omissions are much more rampant in organisations where these functions are in silos, and much more challenging to rectify once they build up over reporting periods.

Conclusion: Actionable Insights for Finance Professionals

The IFRS 2 is a standard that favors preparation and discourages short cuts. To those in the finance sector, at any level of their career, the need to establish a strong foundation on the topic of IFRS 2 stock options is becoming increasingly important as equity-based compensation gains popularity in all industries, geographical locations, and company sizes. The requirements of the standard are definite, the application of the standard is a matter of genuine technical judgment and the effects of non-observance of the requirements are extremely tangible in the shape of audit findings, restatements or scrutiny by the investors.

The most valuable practical actions that you can make are started far earlier than the first one can be offered. Having defined grant date practices, investing in sound employee stock option administration systems, and creating a documented way of ESOP fair market value determination at the beginning will save your organisation a lot of time and money when the auditors come. In the case of unlisted companies in certain instances, the temptation to not fully comply with formal IFRS 2 until it is desperately required often at the most opportune time, should be strongly discouraged.

In the profession of building a career in financial reporting, transaction advisory, or equity compensation, knowledge of IFRS 2 opens up. Organizations periodically hire staff that has the capability to handle the entire cycle: plan design and valuation through to journal entry, disclosures and audit liaison. The ones who know not only the machineries, but the judgment or how to apply this or that model of valuation when and where, the treatment of a vesting condition, to treat a modification is always in demand within any finance team. In a field where technical accuracy and field experience would seldom converge, individuals who invest in the creation of both will find that experience in IFRS 2 stock options is a long-term and sellable professional benefit.