How Are Stock Options Valued in Private Companies?

Understanding How Are Stock Options Valued in Private Companies?

Stock option valuation in private companies is used to calculate the fair market value of stock options that are reported on the financial statements, for tax planning and for employee compensation. Private company valuations are based on models like Black-Scholes, private binomial models or the option pricing model framework outlined in the 409A valuation requirement, which are not available in public companies where share prices are observable. Such valuations are imperative for adhering to IRS guidelines, exact GAAP bookkeeping and open with stakeholders. Valuing options and assigning values to equity options when setting up an ESOP or withholding options are assigned to employees means that you will be aware of the value of the options and that you are being fair, that you are doing the right thing and that you are making informed business decisions at every stage of your business growth.

Key Takeaways:

- Common stock valuations, typically performed under the 409A rules, are necessary for private companies issuing equity and must be done correctly, or employees may face tax penalties, and companies can be liable.

- The Black-Scholes model and binomial models are the models commonly used in the industry for calculating the fair market value of stock options, which include variations in exercise price, time to expiration, volatility and risk-free rates.

- The value of equity options valued in private company transactions is very sensitive to the equity assumptions, such as discount for lack of marketability (DLOM), discount for lack of control (DLOC) and probability-weighted scenarios.

- The 409A valuations are reviewed annually or for any significant change in the business fundamentals or an acquisition event, which is required for equity compensation reviews and valuations for ESOP plans.

- Well-executed stock option valuation helps employees avoid unexpected taxes, ensures fair stock option grants and shows investors and acquirers the governance development of the company.

What Triggers the Need for a 409A Valuation?

A 409A valuation requirements process starts when a private company issues equity compensation, such as stock options, restricted stock units (RSUs) or restricted stock awards (RSAs) to employees, contractors or advisors. Private companies must have a certain exercise price for stock options, which must be set at or above the fair market value of the underlying common stock on the grant date. If the exercise price is under the fair market value, the employees who get the options will immediately have to account for the difference as compensation income and will be taxed at the prevailing ordinary income tax rate. In addition to personal exposure, companies with options that have exercise prices that are below a compliant valuation may be subject to penalties, audits and liability from affected employees. So, private companies are required to have an independent qualified valuation before offering equity awards, as required by 409A.

The need for valuation is not just in the context of initial equity grants. If a private business makes material business changes (such as a key executive departure, significant funding round, key customer acquisition, a significant market shift or a significant milestone in revenue), then a new valuation is advisable. Most businesses will perform annual 409A valuations to ensure they are up-to-date with the valuation, particularly if they are in growth stages where the valuation will vary from year to year. Moreover, when companies are approaching an acquisition or public offering, they need to have new and fresh valuations that can support financial disclosures and tax reporting that are both credible and valid. The failure to do this critical task can result in downstream issues: tax audit problems years after option grants, inability to close acquisitions when valuation documentation is insufficient, or equity compensation programs accidentally become out of compliance with regulations.

How Is Fair Market Value Determined for Private Company Stock?

The methodology used to determine the fair market value of stock options in private companies is unique since there are no market-traded prices available, unlike public companies. Valuers use a variety of methods: the income approach (discounted cash flow, or DCF, models which attempt to estimate future earnings, and then discount them to present value); the market approach (which entails relating the value of the firm to that of similar publicly traded firms or the multiples paid on recent acquisitions); the asset-based approach (whereby the value of the firm is based on assets, particularly those in the assets-rich industries). In the case of predictable cash flow and a stable and well-defined growth curve, the income approach is usually the more dominant approach in valuation analysis, particularly for private companies. If the cash flow of the venture is more uncertain, with little or no history of dividends, then the data from the market method can be used more heavily by the valuer, who will use comparable valuations of other venture-backed companies or the prices that other companies have received in recent stake sales to value the venture.

After the overall enterprise value is determined, values need to be distributed amongst the capital structure. Private firms usually have more than one class of stock (common and preferred), with analysts having to value the common stock portion (which is owned by employees and option holders). In this valuation, the liquidation preferences and cumulative dividends of the preferred shareholders are subtracted from the enterprise value. The residual value is distributed proportionately amongst the stockholders, representing the shares they hold. The critical judgment areas added to this process are the assumed discount for lack of marketability (DLOM) and the discount for lack of control (DLOC) (usually 25–50% for private companies). These discounts (and the reality that private common stock does not have the same liquidity or control as public common stock) explain the existence of these discounts. Each assumption and methodology is adequately documented in a credible valuation report, which will be auditable by the IRS and will enable employees to feel confident in the fairness of their grants of stock options.

What Models Calculate the Value of Stock Options?

The Black-Scholes option pricing model is the most commonly used option pricing model to calculate the fair market value of stock options that meet the requirements of 409A. The Black-Scholes option valuation model was developed in the 1970s for traded equity options, with five key inputs: the current stock price, which is based on the 409A valuation; the exercise price of the option; the time to expiration of the option (often 10 years for equity options); the risk-free interest rate (typically the 10-year Treasury rate); and the volatility of stock returns. The value of the options is calculated by the model as a per-share value and then multiplied by the number of options granted to determine the total value of the options granted. The reason for this is that a 10-year option on a private company with a 40 percent volatility (typical for a tech company) and a 2.5 percent risk-free rate could be worth $18 per share, if the valuer estimates that the fair market value of the private company is $50 per share. This employee has 10,000 options; based on the model, they have earned about $180,000 so far.

The Black-Scholes Model is ubiquitous, but the binomial option pricing model is more flexible in the case of more complex scenarios, such as options with time-varying parameters, early exercise patterns, and unusual vesting schedules, etc. The binomial model is based upon a tree of possible stock price movements over time, with option values calculated at each node depending on the probability that the stock price moves up or down. This method more adequately reflects the fact that the value of Private Companies can decline and appreciate at significantly different rates: VC-backed firms can appreciate in value quickly (upward arrow), or they can lose value if product-market fit doesn’t materialize (downward arrow). Also, a valuer can make use of probability-weighted scenario analysis if there is extreme uncertainty: base case (continued operations), upside case (successful exit or introduction of a new product), and downside case (lower revenues or restructuring). There is a probability weight associated with each scenario, and the option value is the weighted average of the outcomes. They are more advanced and will only work with a seasoned valuer, but will offer enhanced credibility and defensibility for equity compensation programs.

How Do Discounts for Lack of Marketability and Control Affect Valuations?

One of the most important aspects of the analysis of 409A valuation requirements is the use of discounts based on the inherent limitations in private common stock. Discount for lack of marketability (DLOM) recognizes that a private stock is not immediately marketable like a share of stock in a public company. Private company investors should be willing to pay anywhere from 25% to 50% (or even more) to account for the illiquidity of the investment, as well as the uncertainty of when and whether there will be any liquidity events. A software start-up that is coming to a Series B round may apply a 35% DLOM, which assumes the high likelihood of a liquidity event (investment round or acquisition) in the near future. On the other hand, a private company that is stable and profitable, but has no immediate exit strategy, can use a 45% DLOM, which reflects lower near-term liquidity expectations. The second discount for lack of control (DLOC) is applied in the valuation of minority interests that do not have control over them, either because they have a minority interest or lack any board representation. Employee option holders do not have direct influence over the company; therefore, according to the assumptions for the value estimation of options, a slight DLOC (10-20%) may be applied if the option value estimation involves decisions to be made at the level of company control (such as an acquisition or dividend policy).

These discounts are not random discounts, but rather discounts based on empirical evidence, precedent transactions and industry methods. Valuers look at studies on private equity transactions, restricted stock transactions, and similar company analyses to determine the level of discount. While a higher DLOM might be justified for a pre-revenue biotech firm with a 10-year drug development cycle, it’s a more difficult case to make for a cash-flowing SaaS business that’s serving recurring monthly income. Discount applications are closely examined by the IRS and auditors, and any discounts that are excessive or for no valid reason are subject to audit flags. Best practice is to keep a record of the rationale behind the choice of discounts, and provide a basis for this, such as market data, company factors and industry benchmarks. Transparency of assumptions regarding discounts to employees and stakeholders is seen as evidence of governance maturity and minimizing compensation-related disagreements down the road.

What Are Common Challenges in Stock Option Valuation?

There are a number of recurring issues in valuing stock options in private companies. First, it is hard to project future cash flows when not a lot of financial information is available in the past, especially in the case of startups or businesses that are rapidly changing. The reality is that growth rates need to return to “normal” for a five-year-old SaaS company that is growing at an explosive pace, but to make such an assumption is to overvalue the company’s valuation and option values, leading to future problems with valuation impairments or audits. Second, inputs to the Black-Scholes model to determine appropriate volatility are subjective. The valuation of private companies does not have the benefit of a price history in the public markets; instead, private company valuers use the volatility of publicly traded companies that are similar to the private company being valued, industry volatility or, in some cases, judgment based on the risk of the company. Tech startups typically have volatility estimates of 30-50%, and defensibility must be based on a transparent methodology and consistent application. Thirdly, it is less reliable to use the market approach because there are no external market transactions. Valuers refer to recent funding rounds (which may mean they’re valuing the firm from a different investor’s point of view or that they were valuing the firm with a strategic premium that wouldn’t be mirrored in a standalone valuation), M&A transactions (which may include a synergy premium that wouldn’t appear in a standalone valuation), and IPO comparables (which may or may not be relevant to the private company being valued).

A fourth challenge comes when the situation of a company changes very quickly. A private company that raises a well-rounded Series A round with outside investors might find that it needs to raise the valuation of its 409A, possibly on rounds after that, up to two or three times the amount of the first round. This helps the holders of the options, but it could cause some problems: options that were given (exercised) 2 years ago went for $20, but are now worth $50 per share, which is not fair. On the other hand, a company’s growth can stall and/or market conditions could deteriorate, causing valuations to fall and leading to impairment charges, and maybe even restricted stock unit clawback provisions. Fifth, equity compensation practices are complex to coordinate in terms of valuation updates. Companies will need to have current cap tables, know the dates of options granted as compared to the date of the options’ valuation, and make sure that the exercise price was determined in accordance with the then-existing valuation. Too little documentation (no valuation reports, ambiguities in grant agreements or common stock definitions) poses compliance challenges years after the options are given when employees or auditors doubt that option grants complied with 409A requirements.

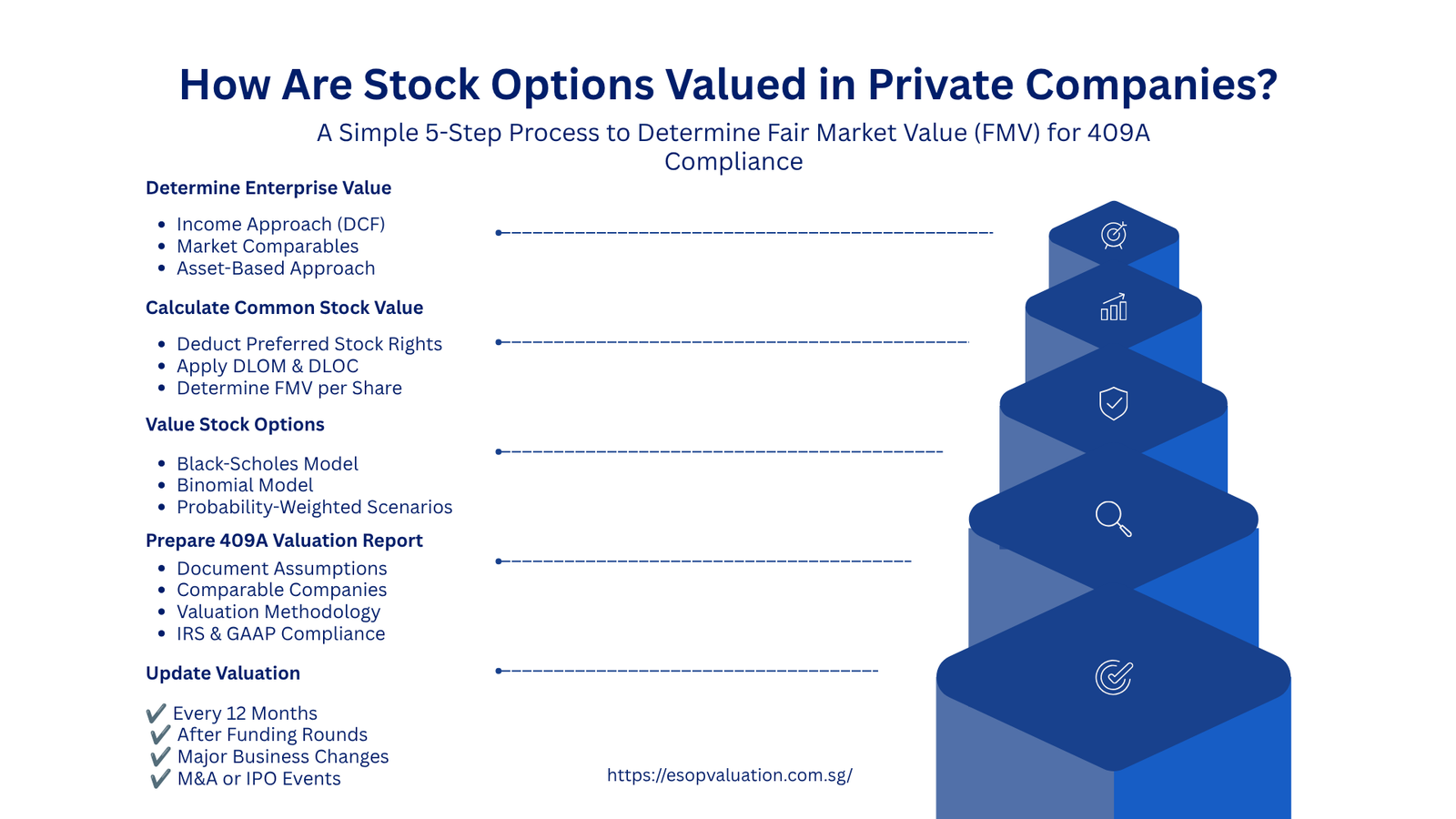

Five Essential Steps in Valuing Stock Options for Compliance

- Step 1: Identify Enterprise Value—Estimating the overall value of the enterprise using income, market and asset approaches, including financial projections, comparable multiples and risk-adjusted scenarios.

- Step 2: Assign Value to Common Stock – deduct preferred stock liquidation preferences and cumulative dividends from enterprise value; apply discount(s) (DLOM/DLOC) to determine FMV per common share.

- Step 3: Select and Apply Valuation Models: Apply Black-Scholes, binomial models, or probability-weighted scenario analyses to determine the value of options, given assumptions of exercise price, terms, volatility, and risk-free rate.

- Step 4: Document Assumptions and Methodology—Develop detailed valuation reports using clear methodology, sources of data, comparable company valuation data and discount justifications to meet audit compliance requirements and be defensible for IRS purposes.

- Step 5: Update Valuations Annually and After Material Events—Refresh 409A valuations yearly or when significant business changes occur to ensure ongoing compliance and fair equity compensation practices.

Table 1: Fair Market Value Stock Options: Sample Valuation Comparison – How Are Stock Options Valued in Private Companies?

| Company Stage | Fair Market Value/Share | Option Volatility | DLOM Applied | Option Value/Share |

| Seed/Pre-Seed | $2–$5 | 55–70% | 45–50% | $0.55–$1.50 |

| Series A | $15–$35 | 45–55% | 35–40% | $4–$10 |

| Series B/C | $40–$100 | 35–45% | 25–35% | $12–$35 |

| Late-Stage/Pre-IPO | $150–$500 | 25–35% | 15–25% | $25–$150 |

Real-World Case Study: Mid-Stage SaaS Company 409A Valuation

A startup that was founded 4 years ago and had raised a Series B investment round 8 months prior was valued at $75 million. The Company was nearing the annual bonus cycle and was considering giving stock options to 45 employees. The CEO discussed with the company’s legal counsel the requirements for a 409A valuation and found that the company had a Series B valuation, but this was based upon the price paid to the investors (which included control and marketability premiums) and not the fair market value for the employee options. We had the company hire a third-party valuation company to conduct a compliant 409A valuation on the common shares.

The first step in the valuation analysis was to estimate the enterprise value. The firm applied a discounted cash flow (DCF) analysis to estimate the company’s annual recurring revenue (ARR) to be $35 million in five years, increasing from $12 million in the current year, while also forecasting greater operating margins of 25% as the company scales up from 10%. The firm then compared the trading multiples of similar-stage public SaaS companies and came to the conclusion of an enterprise value of $95 million. There was $15 million in preferred stock liquidation preferences that the company had outstanding from the Series A and B rounds. So the residual value attributable to common stock was $80 million. The valuation team, however, calculated the fair market value of common stock after applying a 35% discount for lack of marketability (which seems appropriate in this case, since the company had no exit opportunities known to the valuation team) and, in light of the company’s capital structure, to be $18 per share.

The valuation team applied the Black-Scholes model values to the company’s $18 stock price, 40% volatility (which is calibrated to other public SaaS companies in the same growth phase), a 10-year term on the options and a 2.4% risk free rate, to determine the fair value of the options with an exercise price of $18. The company’s board granted options to all eligible employees based on the $18 common stock fair value and $8.60 option value as determined by the 409A valuation. Equity compensation valued at about $43,000 ($8.60 × 5,000) was awarded to an employee with 5,000 options. Importantly, the company conducted a compliant valuation at the grant date, which was used to establish the exercise price, thus avoiding the risk of employees facing potentially large tax liabilities due to the lower exercise price and the company facing IRS audit exposure. 18 months later, the company takes in a Series C investment of $200 million. 18 months later, the company closes a $200 million Series C funding round. This was reflected in a new 409A valuation, where common stock was valued at $58 per share, a 222% rise. If the company hadn’t been careful to value the stock of its 409A grants at each stage of funding, the subsequent 409A valuations would have revealed that it had been undervaluing the stock in the past, leading to awkward compensation equity issues and potential employee grievances.

This case provides an example of the importance of ESOP valuations and continuous 409A compliance – it demonstrates fairness towards employees, and institutional knowledge is gained that can speed up future fundraising, M&A processes and exit planning. Those that value it as a governance principle, rather than a checkbox once a year, create trust among stakeholders and safeguard against compliance shocks.

Key Challenges and Lessons Learned in Stock Option Valuation

Businesses which issue stock options have to deal with a number of ongoing difficulties in keeping their valuations compliant. The first obstacle is the cost and the time. An independent valuation with a qualified firm will generally range from $5,000 to $25,000, depending on the complexity of the company and the amount of analysis that is needed. Having someone invest money into your startup can be a strain for the early-stage business with limited capital, especially when the business has not yet made a profit. But the costs of skipping or delaying valuations are much higher, however: employees who get tens of thousands of dollars in tax bills when they’re not expecting them, companies unable to raise follow-on financing because they don’t have the proper 409A documentation, or option holders filing lawsuits claiming that the valuation is unfair. Investing in professional valuation early provides benefits in terms of risk management and stakeholder goodwill.

The second challenge comes from the fact that employees have expectations, but valuation isn’t what they might believe. If a business issues options at $10 a share and a later round of funding puts preferred stock at $50 a share, the employees will be angry—they feel diluted, or there were some mistakes in the valuation of the earlier round of funding. Indeed, this situation can only be explained by the proper use of a discount on lack of marketability for common stock, and the investments of preferred shares at premium prices are a reflection of the control and certainty of investment, which are not available to holders of common stock. Explain the value process and why they are used in a clear and transparent way, which will reduce the skepticism of employees. Firms which teach their workers on option valuation, and record the grounds in valuation reports provided to the equity holder population, increase trust and minimize grievances.

The third lesson relates to the need to keep updating valuations regularly. If a company is undertaking 409A valuations on an irregular basis, such as when seeking to raise capital or in connection with an acquisition, then it could possibly have a number of years with no documentation. If there are any periods of undocumented option grants, and an audit or litigation takes place after, the company has no evidence of fair market value at the option date. IRS examiners can question the grant prices as unreasonable, which can result in back taxes and penalties for employees impacted. Best practice requires that valuations should be updated annually (preferably in line with annual equity grant cycles), with up-to-date documentation of each grant. In addition, companies should have an equity grant protocol that includes a checklist that ensures exercise prices are always at or above the most recent fair market value determination, option agreements specifically reference the valuation authority, and vesting schedules are consistent with company retention goals. Good governance in equity compensation helps to resolve future conflicts and act in a mature way towards investors and acquirers.

How Are Stock Options Valued in Private Companies? – Conclusion

Valuation of stock options is not a compliance activity, but an essential part of private company equity compensation fair practice. The 409A valuation requirements are intended to safeguard employees against unfavourable tax results and to provide a predictable and consistent approach for valuing 409A stock options. By addressing valuation as a governance matter, redoing it annually, hiring qualified independent valuators, and providing clear communication to the option holders, businesses can develop stakeholder trust, lower compliance risk and plan for a successful fundraising and exit.

Finance leaders facing equity compensation at private companies have several action items:

(1) If not in the past 12 months, take advantage of the opportunity to commission an independent 409A valuation; (2) If there have been material changes in the business, have it done. (3) Implement a standard policy for equity grants that will include a requirement for the exercise price to be at or above fair market value based on the latest valuation. (3) Record all valuation assumptions, methodologies and conclusions on written reports, which are kept with your equity records. (4) Train staff on option valuation and route to liquidity to boost engagement and retention. (5) Discuss with a tax adviser the tax consequences of your options for the company and the employee. (6) When conducting an acquisition or valuing for an ESOP valuation, make sure there are up-to-date 409A valuations in place to speed up due diligence.