How Should Startups Design an Effective ESOP Plan?

A practical guide for startup founders, finance professionals, and job seekers entering high-growth companies

Understanding How Should Startups Design an Effective ESOP Plan

An Employee Stock Ownership Plan (ESOP) is a benefit that allows startup employees to buy shares at a predetermined price, making their financial goals similar to the company’s long-term objectives. A thoughtfully designed ESOP can be one of the most effective methods for a startup to recruit, retain and incentivize employees – if designed properly. In this article, the founder and the finance team will cover the critical decisions they need to make: how much equity to reserve, how to calculate the fair market value of an ESOP for startups, how to divide the equity grants among roles and seniority and how to explain the plan in a way that can truly be a competitive advantage.

What Is an ESOP and Why Does It Matter More for Startups Than for Established Companies?

An ESOP (typically used in the start-up arena as a stock option plan) gives employees an option to purchase a certain number of shares in the company at a specific rate (the exercise or strike price) after a vesting period. The economic value comes when the company expands, and the value of the shares is higher than the strike price: When the employee sells his shares at the lower historical price and when he trades them in a liquidity event, like an IPO or merger, the difference is considered a profit; in some cases, he might also make a profit from a secondary trade. The potential for wealth creation of a well-designed ESOP is in the difference between the strike price and the share price at the end of the day.

The ESOP is of immense value to a startup and cannot be replaced by cash compensation. Usually, a start-up firm won’t be able to compete with those of established employers when it comes to remuneration, and the prospect of working for a firm that isn’t profitable or even at the bottom of the market yet is still high risk. That risk asymmetry is balanced by equity in the form of options — options that allow them to be a part of the upside they’re helping to build. A well-designed ESOP can also help to create a sense of ownership, which can boost the engagement of employees and improve their overall job performance. When everyone on the team is involved in the company’s success, the ’employee mindset’ and ‘owner mindset’ bridge over the issue of compensation. That is why startup ESOP plan best practices view the plan as more than a financial tool – it is a cultural and strategic tool.

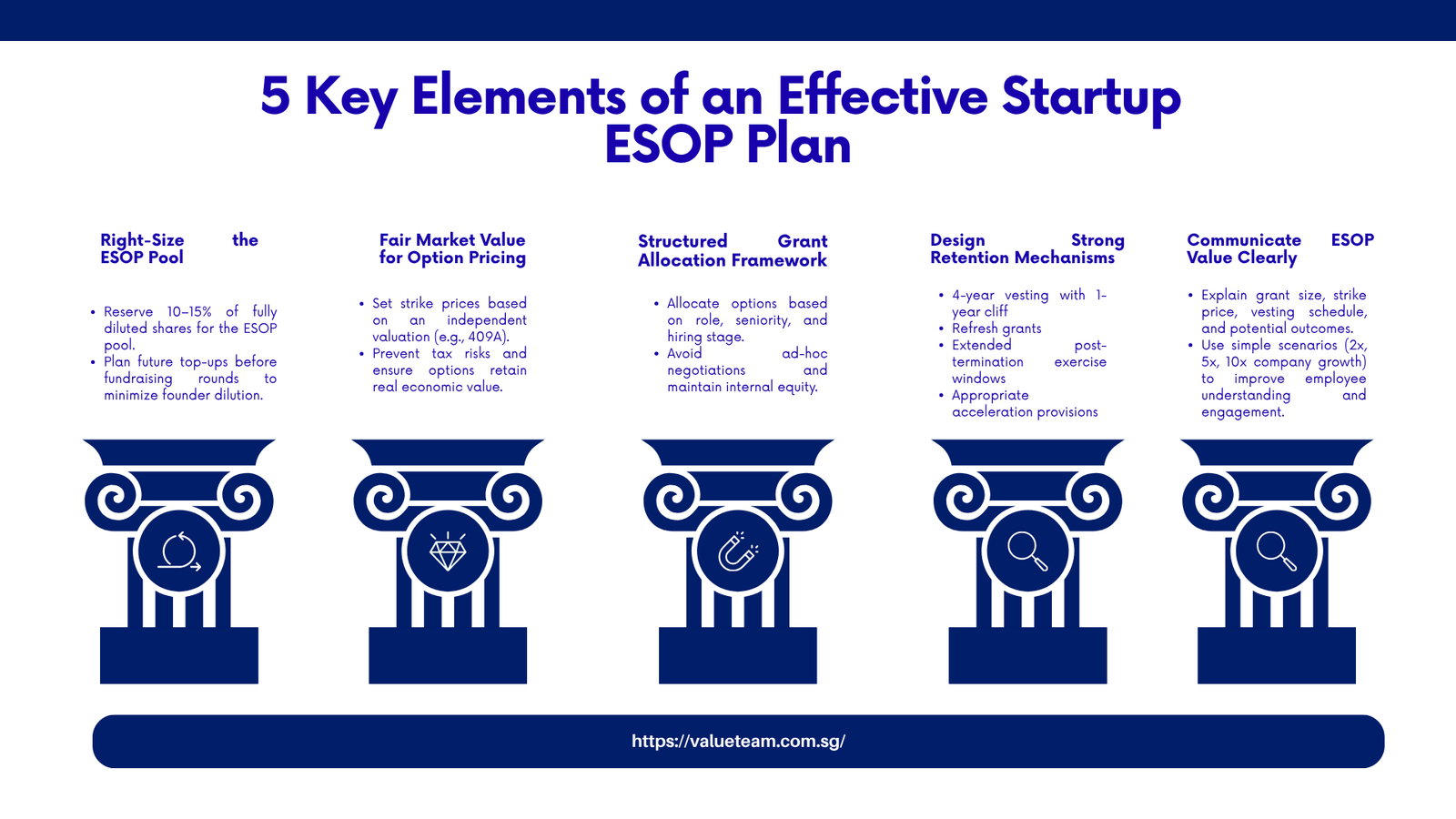

How Much Equity Should a Startup Reserve for Its ESOP Pool — and When Should It Be Topped Up?

The sizing of the pool is the first major decision in the design of an ESOP and has ramifications throughout the life of the company. The typical early-stage startup sets up an ESOP pool of 10-15 percent of fully diluted shares at or shortly after its incorporation. This range shows the competing pressures founders have to deal with: a small pool results in frequent top-ups that lead to dilutions and makes it more difficult to manage the cap table, while a large pool dilutes the founders and the early investors without any need. The exact size will vary based on the speed of the hires, their level of seniority within the organization, and the expected length of funding.

The size of the pool is important, but so is the timing of the pool top-up. Investor term sheets often call for the ESOP pool to be raised to a certain level on a pre-money basis at the closing of the round, which means the ESOP shares are diluted by the top-up and it’s not going to the new investor. Leaders who grasp this will be better able to negotiate with the founders: they can model an accurate hiring plan; they can show that the hires in the pool are sufficient for a given time window. A key component of start-up ESOP allocation strategy that is often neglected until the time of term sheet. The model-building process is a sign of financial sophistication and a legitimate way to control dilution if one can show investors a realistic picture of the volume of options that will be used over the next 18 to 24 months.

How Is the Strike Price Determined — and What Happens When ESOP Valuation Gets It Wrong?

The price of an option to grant must be fair market value of the underlying shares on the date of grant. In the U.S., this is done with the 409A valuation process: An independent valuation by a specialist firm of the company’s common share value, which serves as a defensible basis for the strike price. Other jurisdictions have similar requirements, albeit that the mechanisms are different. The goal in every case is the same: to avoid having an option with an artificially low strike price which is disguised compensation and thus treated as income at the time of exercise rather than capital gains. With this in mind, it becomes clear that ESOP valuation for startups is not some tedious administrative burden; it’s the way that both the company and the employees can avoid negative tax consequences.

However, when the valuation is incorrect, in either direction, it can cause a lot of problems that can be unwinding. An unexpected and large tax liability can arise for the employee when the strike price is lower than the fair market value, at which point it may be taxed as ordinary income to the employee. If the strike price is too high, it can be the case if the 409A is issued after a large funding round or commercial milestone, and the options will be ‘underwater’ from the time of grant, having no economic value. Employees are discouraged by underwater options and one of the main reasons they don’t value their entitlement to an ESOP. One of the most critical, best practices in the startup ESOP plan that a finance team can implement is to have a current and credible valuation of the ESOP plan, not only when there are regulatory deadlines, but at any significant value inflection point.

What Are the Five Key Design Decisions That Determine Whether an ESOP Actually Retains Talent?

In addition to the size and valuation of a pool, the effectiveness of an ESOP for retaining and motivating employees relies on a series of structural design choices that have been included in the plan document and individual grant agreements. The practical complexity and most of the mistakes are in these decisions.

- Vesting Schedule and Cliff: This has become the standard 4-year vesting period with a 1-year cliff for startups backed by venture capitalists around the world, and for good reason: alignment of incentives with the time between funding rounds, and the cliff to eliminate very early exits before meaningful equity vests. But it involves a conscious decision as to why you’re going against the grain: The shorter the vesting periods, the lower the retention value, and the longer you delay, the more likely it is that someone else will jump in on the competitive talent market.

- Grant Sizing by Role and Stage: A structured ESOP allocation strategy for startups implies that the size of the grant are based on a documented allocation strategy instead of individual negotiation. The grants to employees tend to be higher proportion of the pool of employees hired earlier when risk is large and the company is less valuable. Later-stage hires are given smaller percentage grants, but may receive a larger dollar amount because of the higher share price. Comparing to other companies in similar funding rounds is critical; compensation data providers like Levels.fyi, Carta and Radford offer option grant benchmarks by role and stage as a useful external benchmark.

- Post-Termination Exercise Window: The post-termination exercise window (PTEW) is the time after the employee’s termination during which they have the option to exercise vested options before the expiration of the vested date. The usual 90-day clause is becoming outdated — many employees simply do not have the financial means needed to exercise in that time period, especially if the company has expanded to the point where both the total cost of exercising and the impact of the exercise tax is high. Many startups are now providing longer PTEWs of anything from 1 to 10 years, as extended periods of time can make an option truly valuable, not just theoretical. One area in which the startup ESOP plan best practices have meaningfully developed over the last 10 years.

- Refresh Grants: A founding grant is a grant that is given for more than 4 years. An employee that has served three years with the Company has vested all or substantially all of the grant and has limited equity incentive that has not vested. Refresh grants are additional option grants that are issued during the tenure and thereby cancel out the cliff effect. Companies that don’t have a systematic refresh grant policy are in the awkward position of getting approached by competitors with their most experienced, top performing employees having the least stock grant available to them — who they want to compete with the most.

- Acceleration Provisions: Single-trigger acceleration (vesting accelerates on a change of control) and double-trigger acceleration (vesting accelerates only if there is both a change of control and the employee is terminated or constructively dismissed) are the two main approaches. Double-trigger is more founder and investor friendly because it is not a windfall for employees who are still employed after an acquisition, while single-trigger is more employee friendly but can make deal negotiations with a significant number of employees in the ESOP pool more difficult. The choice of either option should be made together with the legal and finance teams, depending on the stage and target investors of the company.

Indicative ESOP Grant Ranges by Role and Seniority – How Should Startups Design an Effective ESOP Plan?

| Role / Level | Typical Option Grant (% of Pool) | Vesting Schedule | Notes |

|---|---|---|---|

| C-Suite / Co-founder equivalent | 0.5% – 3.0% | 4-year, 1-year cliff | Given at incorporation, associated with long-term commitment |

| VP / Senior Director | 0.1% – 0.5% | 4-year, 1-year cliff | Establish benchmark to series A/B hire norms |

| Senior Individual Contributor | 0.05% – 0.15% | 4-year, 1-year cliff | Correct for limited role in the market |

| Mid-level Professional | 0.01% – 0.05% | 4-year, 1-year cliff | Refresh grants are offered for the 2-year mark common. |

| Junior / Entry Level | 0.005% – 0.02% | 4-year, 1-year cliff | The signal is not an inclusion signal but a motivational signal; at this stage, it is not about building wealth but about getting motivated. |

How Have Real Startups Used Their ESOP Design to Win — and What Went Wrong for Others?

Stripe’s initial stance on equity compensation is a textbook case of how a startup’s equity plan plan best practices can actually help recruit talent. The company was a notable player in providing larger option grants than other companies and communicating them clearly — the company gave detailed information about the company’s valuation trajectory, the assumptions that underlie the value of the option and what would happen to the individual employee’s financial situation should they exit in various scenarios. This transparency was not simply a coincidence, it was a conscious approach that was based on the belief that staff who are aware of the value of what they have are more motivated, more loyal and more effective at promoting the company externally. Early employees had some remarkably good equity outcomes when Stripe peaked at more than $90 billion in valuation—but this was by design, not by accident.

The contrasting lesson from a few high profile startups is the example of those that were less mindful of the ESOP valuation for startups between their major funding rounds. The share price of a company can appreciate significantly without an official funding round when the company’s commercial performance is significantly improved, such as a major customer win, a new product launch or a new geographical expansion. In a few instances, startups that continued the option grant at the old valuation were at great risk of ordinary income tax liability on the portion of the strike price that differed from the new valuation, due to the extraordinary valuation of the company’s next round. The lesson is straightforward but frequently

What Does the End-to-End ESOP Implementation Process Look Like?

When developing an ESOP programme for the first time, finance professionals and founders should be familiar with all of the implementation steps to avoid the most frequent delays and errors. It’s not as simple as it sounds — and the choices that are made in the early stages will impact the flexibility and administrative burden of the plan down the road.

The Six-Phase ESOP Design and Implementation Workflow – How Should Startups Design an Effective ESOP Plan?

| Phase | Key Activities | Output |

|---|---|---|

| 1. Governance Setup | Bring in legal counsel; develop rules, plan; form option committee or board sub-committee | An ESOP plan document approved by the Board. |

| 2. Pool Sizing | Reflect impact of model dilution in expected funding rounds; agree size of pool as % of fully diluted capital | The cap table is capped with the ESOP pool. |

| 3. ESOP Valuation | Get an independent 409A (US) or comparable fair market value assessment, documenting methodology; | Valuation report; strike price set |

| 4. Allocation Framework | Establish grant levels, based on role, seniority and hire stage; Record ESOP allocation strategy for startups. | Grant Policy and Approval Matrix |

| 5. Employee Communication | Draft option grant letters, frequently asked questions (FAQs) and scenario modelling tools for staff | Issue letters of recommendation for employees; create employee education packet. |

| 6. Ongoing Administration | Update valuation at every funding round; process exercises, lapses and refreshes; maintain option register. | Vital data exchange and annual audit; |

Most startups fail to invest enough in the governance setup phase. A vague plan document, which does not provide clarity on how options will be treated on a change of control, does not identify the applicable law for employees in the cross-border context and/or is unclear about the nature of ‘good leaver’ and ‘bad leaver’ status on termination, creates legal and dispute expenses that far exceed the initial legal savings. A good investment that every startup can make in their infrastructure is to hire a specialist equity compensation counsel at this stage, not use a generic template.

Frequently Asked Questions

What is the difference between stock options and restricted stock units (RSUs)?

Stock options give the holder the right to buy shares at a fixed strike price; the financial benefit is the difference between the strike price and the eventual market value. RSUs are a grant of shares (or the right to receive shares) that vest over time without requiring the holder to pay an exercise price — the full market value of the shares at vesting is the employee’s gain. RSUs are simpler and more predictable in value, which is why they are more common at later-stage and public companies. Early-stage startups typically use options because the low current share value minimises the immediate tax impact at grant.

How often should a startup update its 409A or equivalent ESOP valuation?

A 409A valuation is needed prior to any option grant and is typically deemed to be current for 12 months or until a material event.In the United States, a 409A valuation must be performed before an option grant is made, and is said to be current for 12 months or until a material event, whichever comes first. The reasons for a revaluation are material events such as a new financing round or a large acquisition or a significant change in the company’s financial situation. As a practical matter, most growing startups do their 409A routinely every six to 12 months. To implement the best practices of ESOP plans, the valuation refresh should be built into the annual finance calendar instead of being done as a response.

What is a ‘cliff’ in a vesting schedule and why does it matter?

Vesting cliff: Minimum period of time before options vest. With a standard four-year plan and a one-year cliff, none of the options are vested in the first twelve months; 25 percent vest at one year, with the remaining options vested monthly or quarterly for the next three years. The cliff helps prevent dilution due to early turnover of company employees. The cliff is an important commitment hurdle for employees – it’s one of the elements of the structure that has the greatest direct impact on the retention behaviour that the ESOP is geared to produce.

Can a startup change its ESOP plan after it has been established?

Yes, but there are some restrictions. Plan changes typically must be approved by the board, and a few (especially those that would impact the rights of current option holders) may need the consent of impacted employees. Changes that can normally be made via a board resolution include adding a new option pool tranche, changing the exercise window, or updating the plan to adjust for changes in the tax law. If the strike price of options that have already been granted is changed, however, such a change is considered a new grant in most jurisdictions and would require a new valuation. Founders should plan to be flexible from the beginning by incorporating flexibility in the plan document, not in the amendment.

What happens to unvested options when an employee leaves?

Options lapse and return to the ESOP pool on the employee’s termination date. The vested options are exercised during the end-of-term period outlined in the grant agreement, which generally runs for 90 days, but is expanding to longer periods in a growing number of startups. The vested options are only granted to ‘good leavers’ (resigning for good reasons, such as redundancy, sickness) and not to ‘bad leavers’ (dismissed for cause). One requirement of a fair and competitive allocation plan for a startup is its good leaver provisions, and the definition should be clearly set out in the plan rules.

How should a startup communicate ESOP grants to employees who are not finance professionals?

In clear, consistent and with numbers. When you simply say to an employee that they are ‘0.05% of the company on a fully diluted basis,’ that doesn’t really mean anything. Best practices for Startup ESPP plans include making sure each grant recipient has a clear summary that explains the following: the number of options granted, the strike price, the current estimated FMV, the vesting schedule, what happens on exit at illustrative valuations (e.g. at 2x, 5x, and 10x the current valuation), and the key tax implications. Others offer the option of a simple modelling tool available online. The return on investment in clear communication is often huge and gained in multiple ways through increased employee engagement and retention.

What is the typical dilution impact of an ESOP pool on founders?

When a company is incorporated, a 10–15% ESOP pool will result in founders’ ownership of the company being diluted by 10–15% at the time of incorporation on a fully diluted basis. By the time a company progresses to Series B or C, the total dilution from the ESOP can be as high as 20-25% of the total cap table. This is a normal and expected financing and talent strategy of a venture-backed business. Well-thought-out founders who monitor dilution both from the investors and from the ESOP, taking into consideration the life cycle of the company, make better decisions about pool size, grant generosity and when to add to the pool.

Do ESOPs only benefit employees at senior levels?

No, and among the most progressive startups, equity is a purposeful practice in the whole business. The amount of money that can be wagered on a grant is obviously greater for higher-ranking employees, but even a small option grant for the lowly employee is a sign of inclusion, a way to let them know that the company thinks of them as a long-term investment and has a stake in a successful company. The ESOP valuation for a start up is the same no matter if it is a junior employee or a senior employee, the share price appreciated the same will benefit them equally. Having ownership limited to senior levels is a company’s failure to reap the benefits of an actual broad-based ownership culture.

How Should Startups Design an Effective ESOP Plan? : Conclusion

One of the highest leverage investments a startup can make is a well-designed ESOP. It expands the compensation envelope, puts all team members on the same page with respect to the company’s long-term viability, and — when done properly — can be a huge differentiator in a talent marketplace. However, the keyword is “well-designed. A hastily established ESOP, an inconsistent valuation, an unframed allocation, a poorly communicated ESOP will be unable to provide any of those benefits, and may even create legal, tax or employee relations issues that are costly to solve.

The most critical steps for founders are structural, such as: Get a board-approved plan in place early, have a starting pool large enough to cover the next 18–24 months of hiring, have an ESOP valuation for startups before each grant cycle, and document and establish an ESOP allocation strategy for startups that isn’t negotiated on a case-by-case basis. If you’re an accountant or finance pro who is new to a startup, you’ll be in demand right off the bat for your ability to understand option accounting, cap tables, the tax consequences of equity compensation in your jurisdiction, etc. For those looking at a job offer on a startup, the strike price, the vesting schedule, the post-termination window, and the fully-diluted share count are all crucial terms to understand before you accept the offer, and knowing the difference between those terms and knowing what you are accepting with false assumptions. In all three examples, startup ESOP plan best practices are more than just a set of procedures, they are the building blocks of a fair and effective ownership culture.